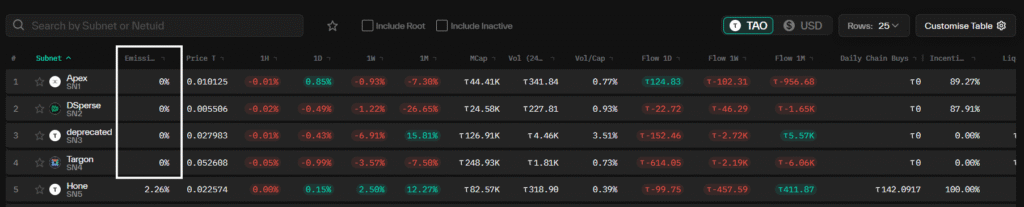

Every few weeks, the same cycle plays out on TAO Twitter: A subnet holder opens Taostats, sees zero emissions on a project they are invested in, and immediately concludes that something is completely wrong.

Tao Templar has six months of operational data showing that this entire reflex is misplaced. Let’s look through it.

The Mechanic Everyone Gets Wrong

TAO Flow controls one specific thing, which is how much $TAO gets injected into a subnet’s liquidity pool, and it does this based on a 30-day exponential moving average of the subnet’s price.

The confusion that drives most of the FUD comes from conflating two things that are actually completely separate from one another:

a. Pool injections are what TAO Flow controls, with $TAO flowing into the pool when investor interest is pushing price upward and slowing or stopping when price is flat or declining.

b. Participant rewards have nothing to do with pool injections, since miners, validators, subnet owners, and stakers continue getting paid in alpha regardless of whether any TAO is being injected into the pool itself.

Zero emissions on Taostats does not mean participants are going unpaid; it means the pool is not receiving $TAO right now, and that distinction is the one most observers fail to make when they reach for doom-and-gloom conclusions.

What Six Months of Data Shows

Tao Templar walked through subnet after subnet on Taoflute and revealed the same pattern across all of them.

This is that emissions are cyclical rather than permanent and that the trough phases are part of normal operation rather than warning signs:

a. Lium (SN51) had strong injections early in its life, then sat at zero emissions for two full months as price declined, until the team executed a buyback and burn that restored sentiment and brought injections back.

b. Chutes (SN64) currently sits at zero injections as price pulls back from earlier highs, though TAO Templar gives it close to certain odds of returning to emissions once underlying sentiment recovers, since the business fundamentals have not changed.

c. Score (SN44) and LeadPoet (SN71) both display the same rhythm of strong injection periods followed by quieter ones, cycling repeatedly without any lasting damage to the health of either subnet.

d. Dsperse (SN2) and Niome (SN55) follow identical on-and-off injection patterns across their full histories, with neither subnet showing any signs of structural decline despite the visible cycles.

The correct timeframe for evaluating TAO Flow performance is the monthly average rather than the daily snapshot. This is because the mechanism itself is built on a 30-day EMA, and judging it by a single reading on Taostats is roughly equivalent to judging a business by one afternoon’s revenue rather than its quarterly performance.

When Zero Is the Right Answer

TAO Flow was not designed to inject $TAO into every pool equally and indefinitely, but rather to stop backing subnets that are not producing anything meaningful, which is a deliberate feature of the mechanism rather than an unintended consequence.

The data on subnets approaching deregistration confirms that this filtering function is working as intended:

a. SN26 received consistent injections while it was active, until the subnet owner executed a large dump that signaled declining conviction in the project, at which point injections stopped immediately and no further $TAO was wasted backing a pool heading toward deregistration.

b. ByteLeap (SN128) shows clear price decline, an absence of code updates, no recent Discord activity, and a negative liquidation haircut of 38%, meaning holders would lose more than a third of their position on deregistration, which is exactly the kind of subnet that should not be receiving any further $TAO injections.

c. SN72 carries a positive liquidation haircut of 10%, meaning deregistration would actually return gains to $SN72 holders. Also, the market is still pricing in that optionality with some injection activity, which is again exactly what a well-functioning allocation mechanism should produce.

The Real Signal

The FUD around TAO Flow comes almost entirely from people treating a 30-day averaging mechanism as if it were a real-time signal.

In reality, it is a slow and deliberate system that rewards sustained investor confidence over time and withholds $TAO from subnets coasting on protocol subsidy without producing genuine output.

Six months of operational data across dozens of subnets confirms that the mechanism is functioning correctly, and the subnets actually worth worrying about are not the ones sitting at zero emissions this week. They are the ones showing zero emissions alongside no activity, no buybacks, and a negative liquidation haircut, all at the same time.

Everything else is just the cycle doing what cycles do.

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment