Seby Rubino presented Zipcode (SN46) at Novelty Search E076, walking through the team’s pivot from real estate appraisal oracles into a full credit oracle network for on-chain lending.

He called Zipcode the ‘bank of Bittensor’ and built the rest of the presentation around that claim. The pitch covered the new Zipcode Finance platform, the partnership with Erebor (Palmer Luckey and Peter Thiel’s bank), the ZIP USD stablecoin, and the vault system that miners compete on.

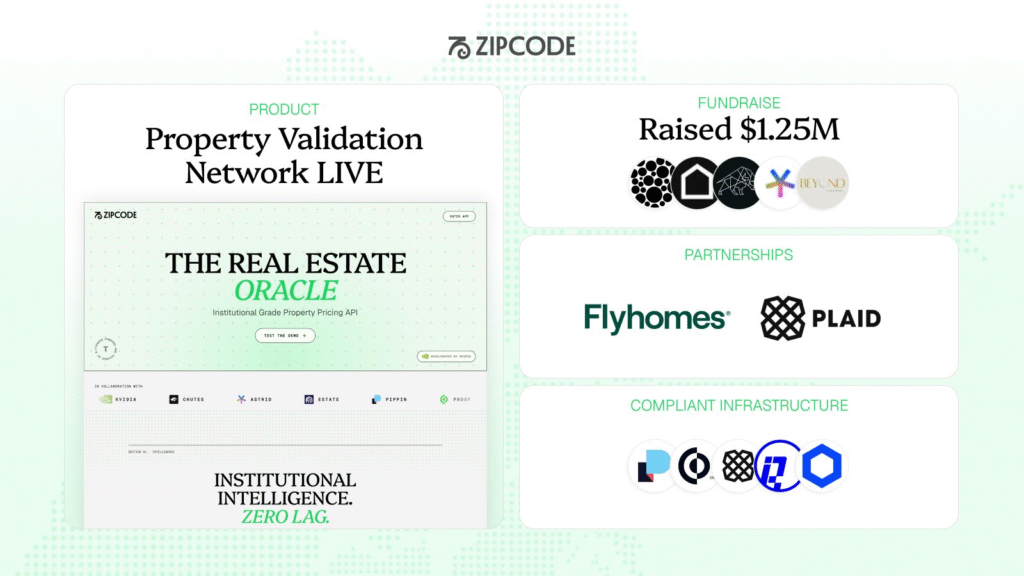

Behind it sits a $23 billion on-chain private credit market that has barely begun to move on-chain because the underwriting is still manual.

The Key Points From the Presentation

What Sebi covered on the pivot, the mechanism, the team, and what comes next:

1. THE PIVOT FROM RESI TO CREDIT ORACLES: Zipcode started as Resi, the real estate appraisal subnet that beat Zestimate and reached 98% accuracy on property valuations. The team is now treating that work as one tool in a larger stack. The argument is that the same approach that solved real estate appraisals can solve every credit verification problem at scale.

2. THE MARKET IS $23 BILLION OF SPECIALIZED ON-CHAIN CREDIT: This is not Aave or Morpho, but private and specialized credit facilities where real-world legal documentation enforces on-chain agreements.

Only 0.1% of the broader private credit industry has moved on-chain because the underwriting is manual and slow.

3. THE FIX IS AUTOMATED TRUST: Zipcode’s bet is that if you can automate credit verification, you can scale on-chain loans the way Chainlink price feeds scaled borrowing, lending, and selling. The system verifies credit standing, income, and signed loan documents through the network, then surfaces those truths on-chain.

4. PARTNERSHIP WITH EREBOR BANK: Erebor is Palmer Luckey and Peter Thiel’s Web3-native bank. Zipcode runs in parallel to Erebor, with each user tracked through a wallet address. The integration with Coinbase Wallet SDK (Software Development Kit) is part of the same stack.

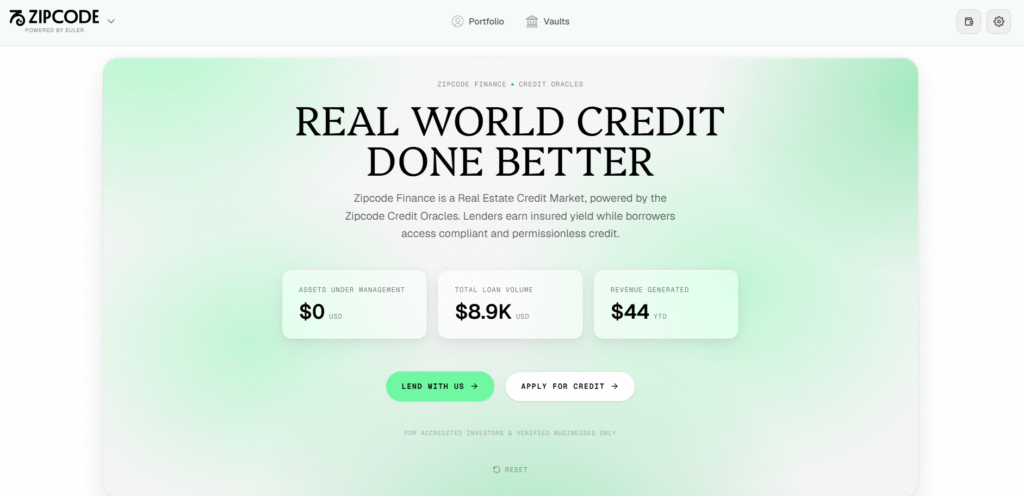

5. THE DEMO ON ZIPCODE.FINANCE: A test net walk-through covered a $500,000 bank deposit at 8% APR, a $500,000 credit line at 6% APR for a borrower, a live notary session through Proof, and DocuSign integration for legally binding signatures. The borrower took out $100,000 and repaid it in the same flow.

6. ZIP USD AS THE TRACKING UNIT: A USD-equivalent token that represents dollar value through the system. It is how Zipcode accounts for where money goes and how vaults are denominated.

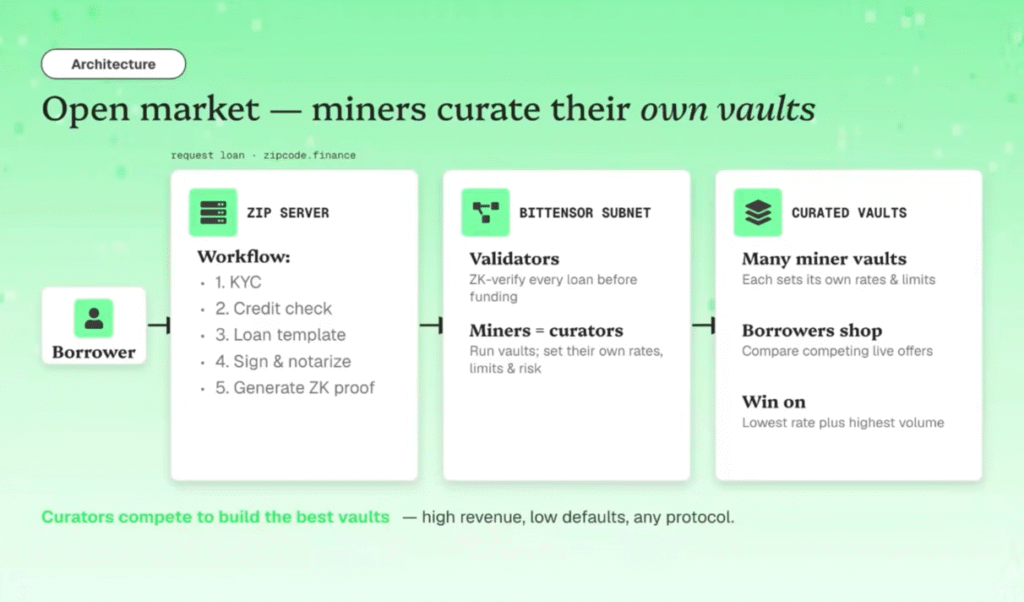

7. THE VAULT SYSTEM IS BUILT ON EULER: Zipcode does not build new vault infrastructure. The vaults sit on top of Euler (similar to Morpho and Compound).

Each vault is a smart contract that holds money, lets users deposit or borrow, and is curated by a third party who sets the terms.

8. CURATORS ARE THE MINERS: Firms like Gauntlet, Alpha Growth, and Stakehouse Capital are the target population. They build the vaults, set the risk parameters, and compete on volume and default rates. The protocol rewards them based on how much volume their vaults generate and how cleanly they manage risk.

9. THE MINER GAME: Move maximum volume with minimum defaults. Balance APY against borrower qualification requirements. Vaults that generate fees and avoid bad loans get more emissions. Vaults with rising defaults lose them.

10. THE VE (VOTE-ESCROW) STRUCTURE: The model works like a vote-escrow system. Like Bittensor’s own TaoFlow, the network tracks money flowing in and out of vaults and routes emissions accordingly.

Token holders can also buy and burn tokens to accelerate emissions on top of the deflationary mechanism already running.

11. THE TECH STACK: A ZIP server runs as an open code base (some API keys hidden) and validators come to consensus on the truth of each loan. A ZK environment built by Dan (who recently joined the team) provides proof-of-proof verification across Plaid, credit scores, and notarization.

12. EXPLOIT PREVENTION: Documentation fraud is handled by Proof. Legally binding signatures mean defaults expose the borrower to lawsuits and credit consequences for seven years. Lenders are insured, so the worst case is a 3-6 month wait for principal and interest.

13. REPLACING THE EXPENSIVE STACK: Proof charges roughly $50 per loan process. Zipcode is positioning to bring that down to $1-$5 by incentivizing subnet-native replacements for Proof, Credit Karma, and Experian over time.

14. PRODUCT EXPANSION ROADMAP: Home loans, car loans, business loans, Polymarket-style speculative loans, and AI agent loans. Collateral-backed loans, including using a house as collateral, are scheduled for an August audit.

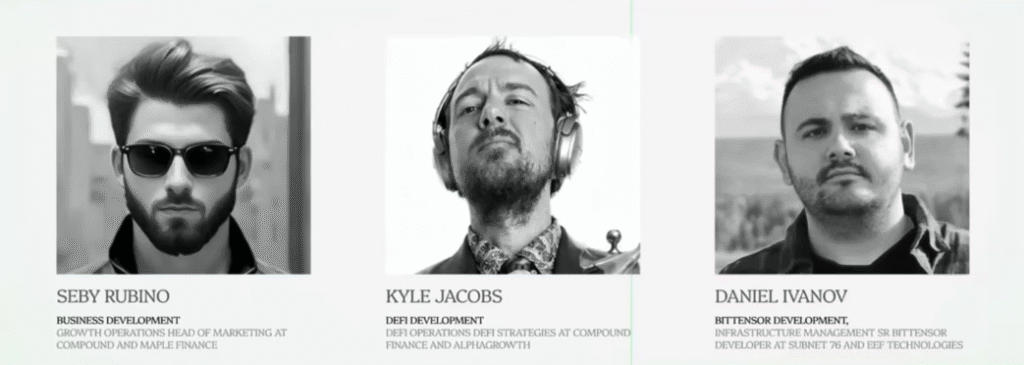

15. THE TEAM: Seby runs the network, Kyle Jacobs (formerly at Alpha Growth and Compound) handles asset strategy, and Daniel Ivanov recently joined to build the ZK (Zero Knowledge) environment.

16. LAUNCH TIMELINE: July 15 is the audited Zipcode Finance launch. The first real estate lenders will receive capital, sign documents, and deposit collateral through the platform from that date.

17. THE RESI MODELS ARE STILL RUNNING: Property appraisal incentives are still live with a dynamic burn. The appraisal work will feed into the larger credit oracle stack as one of multiple tools for processing home-related loans.

18. DITTO MENTION: Seby also runs Ditto (SN118), an agentic frontend product. The Ditto team locked up $300,000 of owner $SN118 during the session, and the Ditto incentive mechanism is being scheduled for its own Novelty Search appearance.

The Bank Play

Zipcode is now building a permissionless credit union conglomerate that scales as more curators bring vaults onto the network. The real estate appraisal work that put SN46 on the map is now one tool in a larger stack aimed at on-chain credit at every layer: personal loans, mortgages, car loans, and eventually agent loans. The bet is that automated trust replaces manual underwriting, the curators compete to bring the best vaults, and the network captures fees on every loan processed through its oracle.

If the July 15 launch works as described, Zipcode becomes one of the few subnets generating direct on-chain transaction revenue from the start. The market it is targeting is $23 billion that has barely moved on-chain. The bank-of-Bittensor claim is ambitious by design, but the substrate to back it sits underneath: the appraisal models, the oracle infrastructure, the ZK proof layer, and the Erebor partnership are already in place. Year two of SN46 is when the rest of the stack gets stress-tested.

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment