Most investors approach Bittensor subnets without a working framework, and the cost of that approach has compounded across multiple cycles.

Michael White returned to the Supercycle Podcast to lay out the one he uses, including a three-bucket allocation system, a quantitative gate around root proportion, and a four-criteria checklist for evaluating new subnets at launch.

The conversation also covered the Conviction score mechanism, the recovery from April 9, and a sharper defense of non-AI use cases than the ecosystem typically articulates in public.

The Frame Michael Brought to the Conversation

The discussion ran from post-April 9 protocol dynamics through to specific subnet reads and the broader defense of non-AI use cases on Bittensor.

The points worth pulling out are below:

a. Bittensor’s recovery from the April 9 Covenant exit has been one of the clearer demonstrations of protocol resilience to date.

The sum of all subnet prices denominated in $TAO collapsed from around $1.40 to $1.25 in the immediate aftermath, then recovered to $1.44 in the weeks since. $TAO allocated to subnets dipped only marginally, from roughly 19% to 18.25%, which signals that trader interest in subnet ‘$ALPHA’ tokens has remained intact even where larger investors have been slower to reallocate.

b. The most consequential proposed change since April 9 is the Conviction score mechanism, which would lock subnet owner $ALPHA for a 21-day window.

The mechanism is designed to give traders advance signal if a founder intends to sell, while preventing the unilateral dumping that occurred with Subnets 3 and 81. The tradeoff is that subnet owners lose some autonomy over their positions in exchange for the protocol gaining a structural defense against rug events.

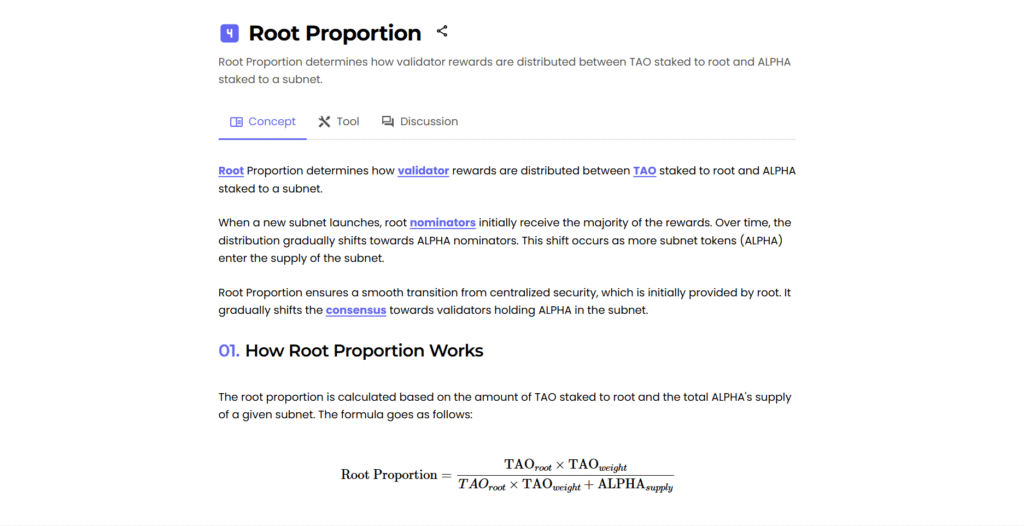

c. Root proportion is one of the most underappreciated metrics for subnet investors. Root proportion measures the percentage of $ALPHA emissions flowing to root holders rather than to $ALPHA holders, and root holders auto-convert those emissions back to $TAO.

High root proportion creates persistent downward pressure on $ALPHA prices. Newer subnets like Subnet 15 (Oro) at over 50% or Subnet 82 at 89% face structural headwinds that established subnets like Subnet 4 (Targon) at 15.5% do not.

d. Michael’s portfolio allocation framework splits subnets into three buckets:

1. Large cap (50% to 60% of capital): established subnets with low root proportion, met teams, and a clear path to revenue. Targon, and Vanta sit here as stable yield plays.

2. Mid cap (25% to 30% of capital): subnets with strong teams where the price has not taken off yet. Zeus and 0xMarkets sit here. Liquidity is thinner, so a single seller can move price 20% in an afternoon.

3. Small cap (10% to 15% of capital): emerging subnets where the thesis is largely the team. Ditto (Subnet 118) and similar early plays sit here, with 5x to 10x upside and a discipline of rotating gains back into large caps as positions appreciate.

e. The dominant trade in subnet investing is increasingly the team rather than the product. Across both the venture capital world and the Bittensor ecosystem, investors are backing founders with prior real-world execution experience over founders with novel ideas alone. The product can be figured out by a strong team. A weak team with a brilliant idea will struggle regardless.

f. Michael applies a four-criteria framework when evaluating new subnets, and Subnet 15 (Oro) is the cleanest current example of all four landing at once:

1. An experienced team with prior execution,

2. Credible backing (Crucible, Unsupervised Capital),

3. A specific, measurable use case (agentic commerce), and

4. Output that translates to other domains over time.

g. Specific subnet reads include Synth (Subnet 50) producing synthetic data with real-world expansion paths into focus group applications,

Ditto (Subnet 118) building agentic memory layers backed by SEBI’s YUGE incubator, and 0xMarkets (Subnet 35) building a native DEX on Bittensor by paying $USDC-locking miners in $ALPHA.

The 0xMarkets design is one of the more clever uses of the incentive mechanism for a non-AI commodity, led by founder Erkin with a deep TradFi and DEX background.

h. The strongest defense of non-AI use cases came toward the end of the conversation. The framing of “this should be pure AI or it does not belong here” is an unproductive purist instinct.

A subnet launch now costs roughly 1,500 $TAO, which is itself a demand signal proving builders want to be here because the incentive mechanism delivers something no other ecosystem can. Capitalism rewards the ecosystem that supports the most diverse set of working use cases, not the one that gatekeeps by category.

The Playbook in One Sentence

Michael’s framework is one of the more disciplined approaches to subnet investing currently being articulated in public. The combination of an allocation framework (large, mid, small cap), a quantitative gate (root proportion), and a qualitative gate (the four-criteria framework) gives investors a working playbook rather than a vibes-based approach to the network.

The harder lesson underneath the conversation is that the protocol itself is still being designed in real time. The signals worth tracking are whether the Conviction mechanism rolls out cleanly, whether root proportion dynamics stabilize across newer subnets, whether the four-criteria framework holds up as more subnets launch, and whether the protocol continues to attract teams with the kind of real-world execution experience Michael is increasingly backing.

If those signals trend in the right direction, the Bittensor subnet ecosystem becomes the most efficient market for AI and non-AI commodity competition currently available in crypto.

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment