Full article by: Andy

Most people still look at Bittensor the wrong way.

They see a token. They see a chain. They see another crypto project.

That’s thinking way too small.

The better way to see it is this: Bittensor is a holding company for intelligence markets. And each subnet is one business inside it.

Once you see that, the whole structure clicks.

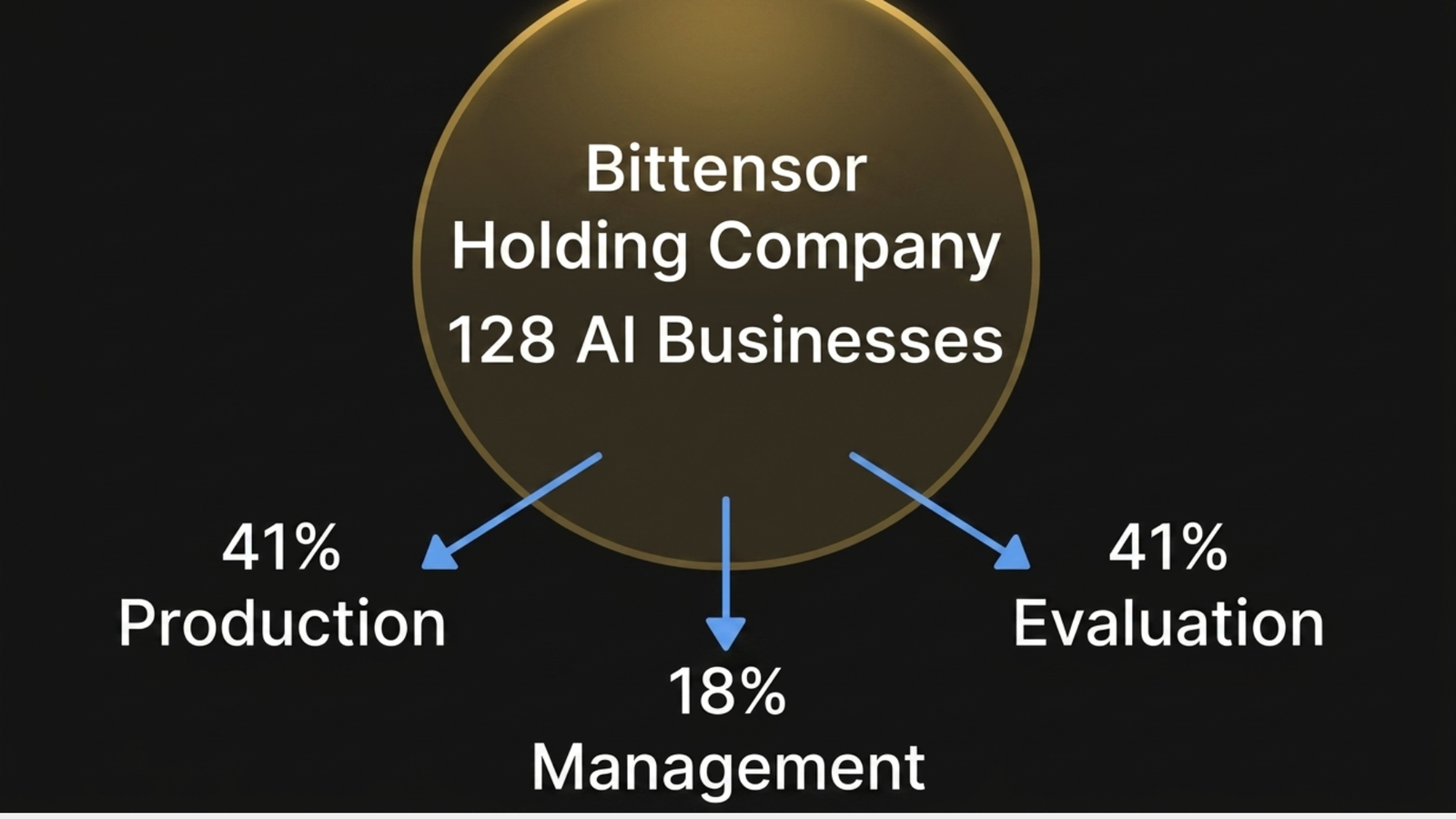

What you are actually looking at is 128 intelligence businesses operating under a protocol-level 82/18 split between production, evaluation, and management.

The 82% side rewards what actually creates value:

- miners producing output

- validators evaluating quality

The 18% side rewards management:

- subnet owners designing and maintaining the business model

Stop looking at it like a blockchain. Start looking at it like a holding company with 128 businesses inside it.

There are currently 128 active subnets on the network. Each one has its own token, its own owner, its own miners, its own validators, its own incentive design, and its own market for capital and talent. That is a portfolio of live intelligence businesses competing under one reserve asset.

The Subnet Owner Is the CEO

Every subnet has an owner. That owner creates the business, defines the rules, and sets the incentive mechanism. In practice, that means deciding what gets rewarded, what gets penalized, and how output quality is measured.

The owner also takes 18% of subnet emissions, which is not free money. It is compensation for creating and maintaining the system that the rest of the subnet runs on. Some owners burn that cut entirely, which is the closest thing crypto has to a founder taking no salary and reinvesting everything back into the business.

The Miners Are the Workers

Miners are the production floor. They do the actual work.

On one subnet that means running inference. On another it means training models. On another it means producing forecasts, writing code, verifying outputs, or doing computer vision.

They receive 41% of subnet emissions, but not equally. They get paid by performance. Their work is scored, and the best miners earn more while weak miners earn less or get replaced. That is a labor market running at machine speed. Just output, scoring, and compensation updating continuously.

And even getting a slot costs capital. Miner registration requires payment and recycling mechanics at the subnet level, which means participation is not free and skin in the game is built into the design.

The Validators Are Quality Control

Validators also sit inside that 41% side of emissions, and their job is to evaluate miner output and assign weights. They are the quality control layer, the independent auditors, and the performance review committee rolled into one.

Weights are what they say about others; V-Trust is what the network thinks of validators’ accuracy. If a validator tries giving a bad miner a high score, the network sees that their Weights deviate from the consensus. The network then lowers that validator’s V-Trust, which directly hits their paycheck.

But here is the key difference from a normal company:

Validators do not just judge. They judge with capital at risk.

Validators need meaningful TAO stake to matter, and their effectiveness depends on how well their scoring aligns with consensus over time. They build credibility through bond mechanics and EMA-based trust, which means they cannot just appear, throw around weights, and dominate instantly. They have to earn influence.

Validators still do this quality control, and their influence is now also tied to Alpha staking with Taoflow as well.

That is a way different quality-control model.

Imagine if every public company’s audit team had to put up its own money and only got paid when its judgments matched the market’s eventual consensus. That is much closer to what Bittensor actually built.

The Stakers Are the Shareholders

When you stake TAO into a subnet, you move TAO into that subnet’s liquidity structure and receive Alpha exposure in return. That means your capital is no longer just betting on the network in general. It is allocating toward one specific business inside the network. Alpha is the subnet-specific token that can be purchased with TAO and tied to that subnet’s economics.

And this is where the structure gets much more aggressive than traditional equity markets.

Since November 2025, Bittensor emissions have been based on EMA-smoothed net TAO flows instead of price. The docs are explicit: subnet emissions now follow sustained net TAO inflows and outflows, with a 30-day half-life and roughly 86.8-day effective EMA window. Subnets with sustained negative flows can eventually go to zero emissions.

That means stakers are not just passive shareholders collecting yield. They are voting with capital on which businesses deserve more resources.

A subnet attracting real stake gets more emissions. A subnet losing conviction gets starved.

No board meeting. Just capital flows measured block by block and smoothed over time.

The Emission Split

The emission split is one of the cleanest structures in crypto, no question.

For every unit of Alpha emitted on a subnet:

- 41% goes to miners

- 41% goes to validators and their stakers

- 18% goes to the subnet owner

That is an 82/18 split between production + evaluation and management. For a network trying to turn intelligence into an open market, that is an unusually clean incentive alignment.

The Burn Dynamic

The burn dynamic matters too.

Bittensor’s tokenomics docs define burned tokens as permanently removed from circulation, while recycled tokens can later be reissued. TAO transaction fees can be burned, and Alpha/TAO mechanics across subnets include both burn and recycle pathways depending on the action. That means the system is not just issuing tokens. It also has mechanisms that can permanently tighten supply.

When subnet owners burn their emissions instead of extracting them, they are effectively telling the market:

I would rather reduce supply than sell today.

That is one of the clearest alignment signals a subnet can send, in most cases.

The Revenue Side

This is where people need to stop treating subnets like crypto. The best subnets are trying to become real businesses, not just emission farms.

Some are doing inference. Some are doing training. Some are doing research agents. Some are doing enterprise verification. Some are doing storage, compute, or agent payments.

And the entire point of Tao Revenue is to track whether real on-chain inflow and burn is starting to offset outflow. Their framework focuses on verifiable on-chain inflow, burn, outflow, and coverage, because off-chain stories mean nothing to token holders if they never show up on-chain.

That is the right way to look at this.

If a subnet claims revenue, the market should ask:

- Where is the on-chain proof?

- Where is the buyback?

- Where is the burn?

- Where is the support for Alpha holders?

Because if that support never shows up on-chain, then it is not yet economic value for investors.

A Word of Caution

That is also why people need to be careful.

Be careful of subnets promising buybacks and never delivering. Be careful of subnets talking about burns without on-chain proof. Be careful of teams that are vague about revenue, vague about customers, or vague about how Alpha holders actually benefit.

And also, be careful of subnets that want public capital and public trust without offering enough accountability around who is actually operating the business.

Not every great team needs to be fully public. But markets do price credibility. And they should.

If we are going to treat subnets like businesses, then people need to underwrite them like businesses.

- Management quality matters.

- Capital discipline matters.

- Transparency matters.

- Long-term alignment matters.

Zooming All the Way Out

You do not just have one company here. You have 128 businesses competing for:

- the same daily emissions pool

- the same stakers

- the same miners

- the same validators

- the same user demand

- the same reserve asset

The strong subnets attract more capital. The weak ones lose emissions and eventually lose relevance.

The registration cost for creating a subnet is dynamic and exists specifically as a barrier to entry tied to demand for subnet slots. That means the network is not passively letting anyone occupy space forever. It forces commitment.

The Covenant Incident and Locked Stake

After the recent incident with Covenant, Jacob’s proposed Locked Stake mechanism adds something traditional markets have always needed.

The CEO of that business now has to prove conviction by locking real $TAO for a visible duration on-chain. Cryptographic transparency around executive alignment.

The idea is simple but powerful: CEO compensation + vesting + lockup discipline.

If passed, it means optimizing management credibility itself.

That is very rare.

Most crypto markets price product. Very few can price time-locked founder conviction.

It’s more like a self-improving capital market for AI businesses.

The Real Picture

So the whole system behaves less like a normal blockchain and more like a live market of competing businesses, all settling through one reserve asset: $TAO

That is the other take.

Not a token. Not just a chain. Not just a crypto project.

A holding company for intelligence markets, where the CEOs are subnet owners, the workers are miners, the auditors are validators, the shareholders are stakers, and the market continuously reallocates resources toward the businesses proving the most value.

That is what people are actually looking at.

And once you see it that way, it becomes much harder to compare Bittensor to anything else in crypto.

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment