Most DeFi platforms talk about being on the right side of the trade, and very few are willing to spell out what that actually costs. That is what makes the latest piece from Erkin Kamran of 0xMarkets worth paying attention to.

Building on his earlier essay arguing that retail traders have been paying rent to brokers for two decades, Kamran has now published the operational counterpart.

This shows a clear breakdown of what liquidity providers on 0xMarkets are exposed to, how the protocol cushions that exposure, and how the economics genuinely compare to a TradFi CFD (Contract for Difference) broker.

Counterparty Risk vs. Market Risk

Kamran opens by separating two terms the community routinely conflates:

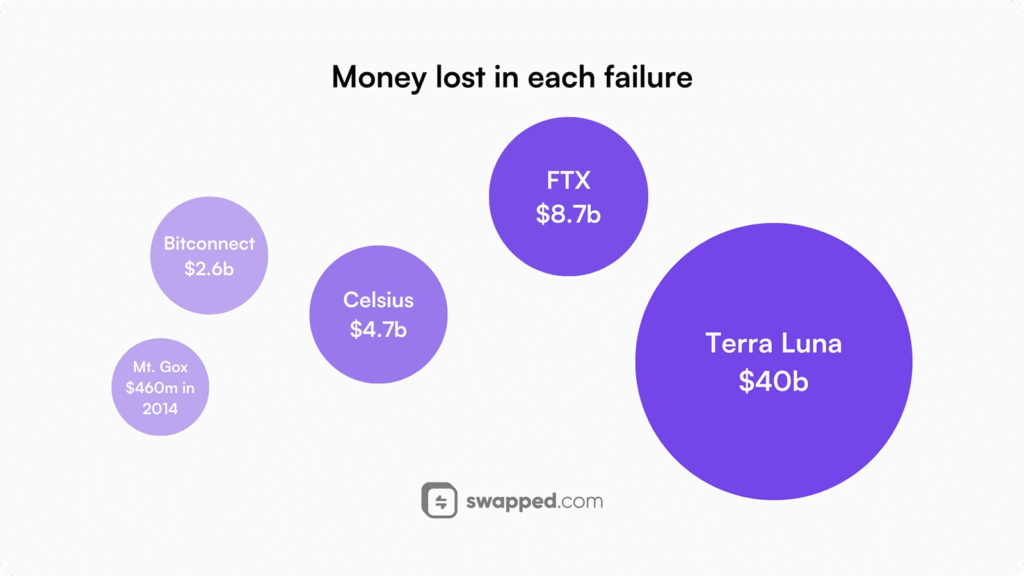

a. Counterparty risk is when the entity holding deposits stops performing. Examples are the FTX, Mt. Gox, and Celsius incidents, and

b. Market risk is the universal exposure every market maker has lived with forever, where positions take hits because prices moved.

0xMarkets is engineered to remove the first by design, and the second is the real LP (Liquidity Provider) conversation.

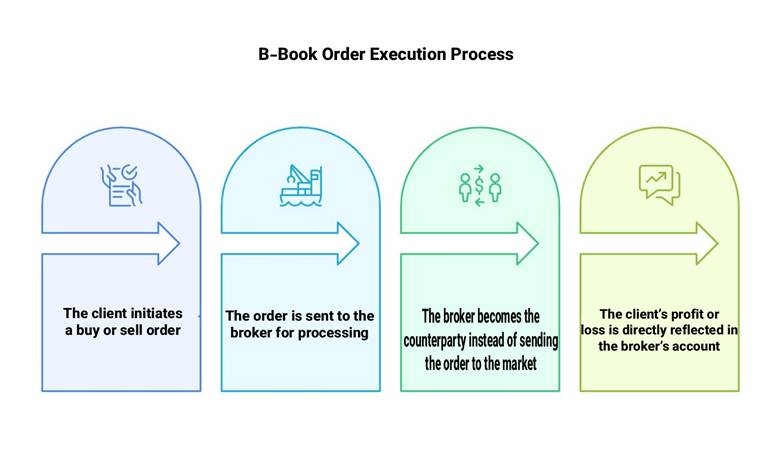

What B-Book Exposure Actually Looks Like

When $USDC enters a 0xMarkets vault, the capital sits opposite the trader book. Kamran names the exposures directly:

a. LPs pay when traders profit, collect when traders lose,

b. Tail events can outpace spread and fee accumulation,

c. A few oversized accounts can move LP PnL more than thousands of small ones,

d. Sophisticated traders running mispriced strategies extract equity over time,

e. Yield is volume-dependent, so quiet markets mean quiet returns,

f. Imbalanced books leave LPs holding the directional opposite, and

g. Early-stage variance is wider until trader populations mature.

These are the inherent character of the role, not flaws to fix.

The Two Layers of Cushion

At the code level, 0xMarkets enforce open interest caps, tiered leverage, skew-based pricing, continuous borrow fees, auto-deleveraging that prevents pool insolvency, an insurance pool funded by liquidation fees, and withdrawal gating during large unrealized trader PnL (Profit and Loss).

At the economic level, the math mirrors traditional broker economics. ESMA disclosures show European retail loss rates between 74% and 89%.

Spread by volume scales linearly while individual trader PnL averages toward zero, and the LP captures the same statistical position the broker traditionally has.

Where the Value Actually Goes

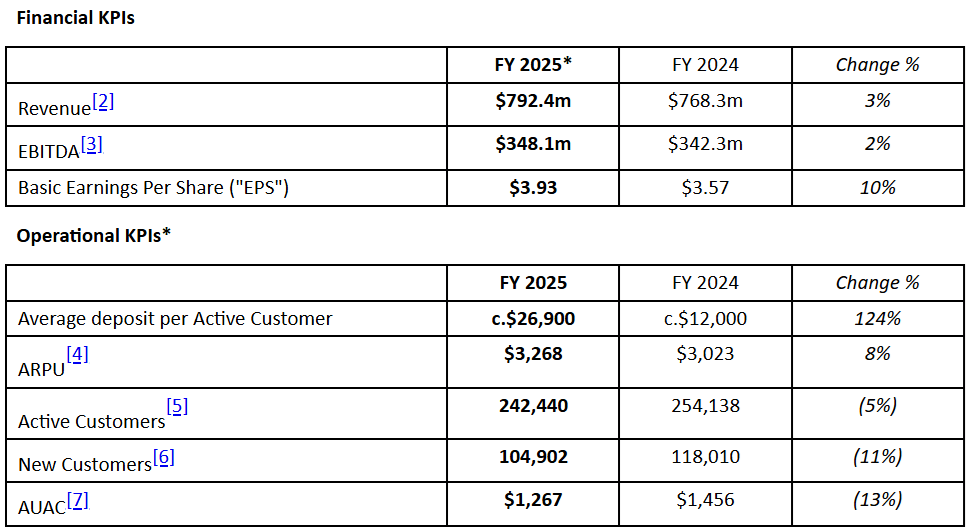

CFD brokers process roughly $1.3 trillion in daily retail volume, and Plus500 alone generated $792 million in 2025 revenue and kept $281 million in profit. The model works, and to Kamran’s question as to who captures the value:

a. In TradFi, the broker captures everything, with shareholders receiving a net-of-overhead slice through dividends, and

b. On 0xMarkets, the structure flips. 50% of trading fees flow directly to LPs, 40% to veALPHA stakers, 10% to treasury, with $SN35 emissions layered on top as yield that does not exist in TradFi at all.

No equivalent product exists in either ecosystem.

The Risks Worth Naming

Other risks are real but not unique to 0xMarkets. These include jurisdictional legal and tax exposure that varies by country and yield type, smart contract risk (Subnet 35 audited by Hashlock, Base contracts pending audit), and oracle risk mitigated through dual-feed redundancy though not eliminated entirely.

The remaining items round out the standard DeFi risk register: systemic risk from Base and Bittensor dependencies, standard market-making withdrawal lockups, governance influence concentrated among large veALPHA holders, and token risk where $SN35 emissions track Alpha’s dollar value while $USDC fee economics continue regardless.

The Real Question

Market risk exists on every market-making book ever run, so the real question is not whether it is present, but whether the reward structure is proportionate to the exposure and whether the protocol’s guardrails cushion the variance meaningfully.

Beyond that, the deeper question is whether any product currently exists, in TradFi or DeFi, that combines broker-grade B-book economics, emissions yield, and on-chain custody in a single position.

Kamran’s answer is that none currently does, and after twenty years of retail sitting on the wrong side of the trade, this is what owning the house actually looks like.

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment