Most crypto narratives are vibes dressed up as theses. Bittensor is one of the rare exceptions where the bull case is arithmetic and math-backed. When you stack the on-chain data side by side, what emerges isn’t a “maybe it goes up” thesis but a structural deflationary spiral encoded directly into the protocol’s mechanics.

The recent article from Andy laid this out clean. Here’s a contextual breakdown of what on-chain data is saying and why every layer compounds the one beneath it.

Layer 1: Exchange Liquidity Is Already Bone-Dry

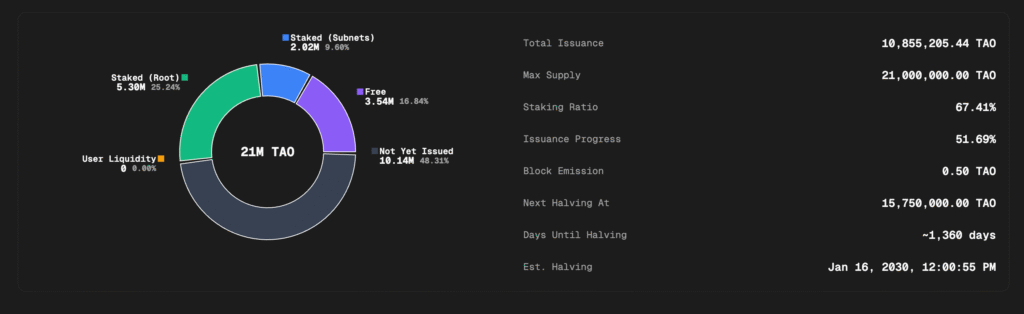

Start with the headline number that should reframe how you think about $TAO supply:

- Total issuance: 10,855,205 $TAO (51.69% of max supply already minted)

- Max supply: 21,000,000 $TAO (Bitcoin-style hard cap)

- On exchanges: ~366,600 $TAO (just 3.4% of circulating supply)

- Staking ratio: 67.44% (7,327,064 $TAO locked)

- Free / unstaked: 16.83% of max supply

- Not yet issued: 48.31% of max supply

At a $250 spot price, the entire global exchange-side liquidity for $TAO is roughly $91.6M. That’s not a deep order book.

The implication is uncomfortable for shorts and beautiful for holders: a single $10M institutional bid would consume more than 10% of available exchange supply. This isn’t a market that requires a narrative shift to move. It requires one buyer with conviction.

Compare this to most large-cap assets where 15–25% of supply sits on exchanges. Bittensor has compressed that to a third of the lower bound, and the trajectory is still tightening.

Layer 2: Reserves Can’t Keep Up With Injections

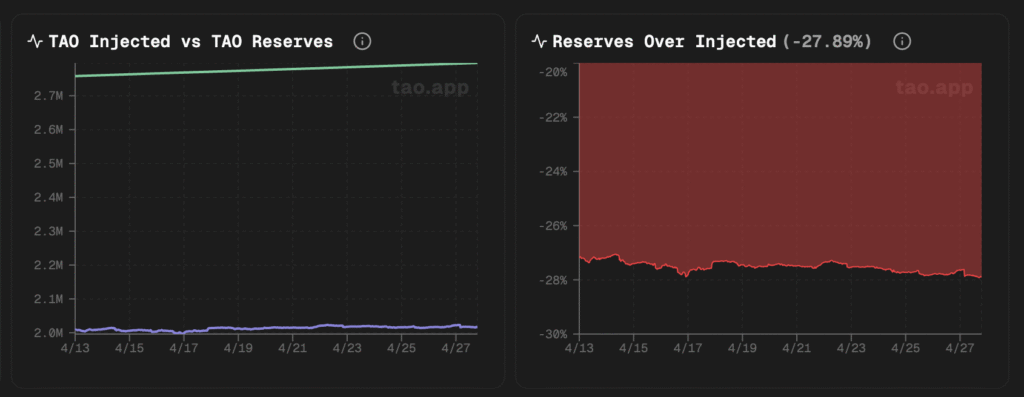

This is the structural deficit nobody is pricing in.

The Reserve vs Injected chart on tao.app shows a -27.89% gap, meaning $TAO reserves are running nearly 28% behind protocol injections into subnets.

- $TAO injected: climbing toward 2.7M

- $TAO reserves: stuck around 2.0M

- The gap: widening, not closing

Here’s why that matters. When the protocol injects $TAO into subnet economies faster than reserves can replenish, subnet alpha tokens become more scarce relative to $TAO demand. That compression drives the alpha/TAO ratio higher, which makes staking into subnets more attractive, which locks more $TAO permanently into subnet-specific stakes.

Layer 3: The Subnet Migration Nobody Is Tracking

If Layer 1 is about scarcity on exchanges and Layer 2 is about scarcity in reserves, Layer 3 is about where all the $TAO is actually going.

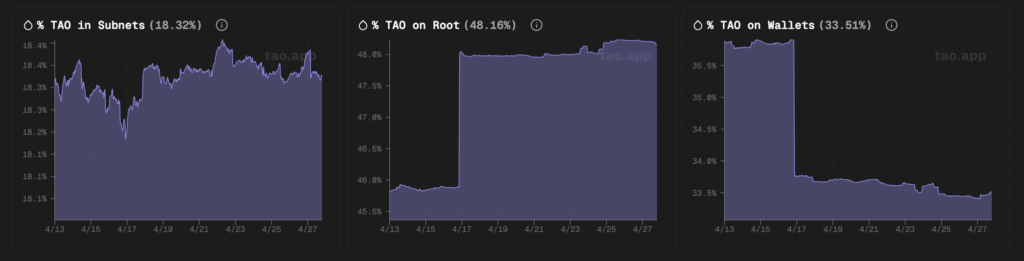

Look at the % TAO in Subnets metric:

- March 2025: ~2% of $TAO in subnets

- April 2026: 18.32% of $TAO in subnets

That is a 9x increase in subnet lockup in twelve months.

The mirror metric, % TAO on Root, tells the same story from the other side:

- March 2025: 75% on root

- April 2026: 48.20% on root

Root-staked $TAO is hemorrhaging into subnet economies and that flow is largely one-way. Once $TAO enters a subnet, it gets converted into alpha, staked to subnet validators, compounded as dividends, and rarely converted back. The friction is real and the incentives are wrong for it to reverse at scale.

This is permanent supply removal across 128 independent sinks, each with its own economy, its own validators, and its own halving schedule.

Layer 4: Subnet Halvings, 128 Rolling Supply Shocks

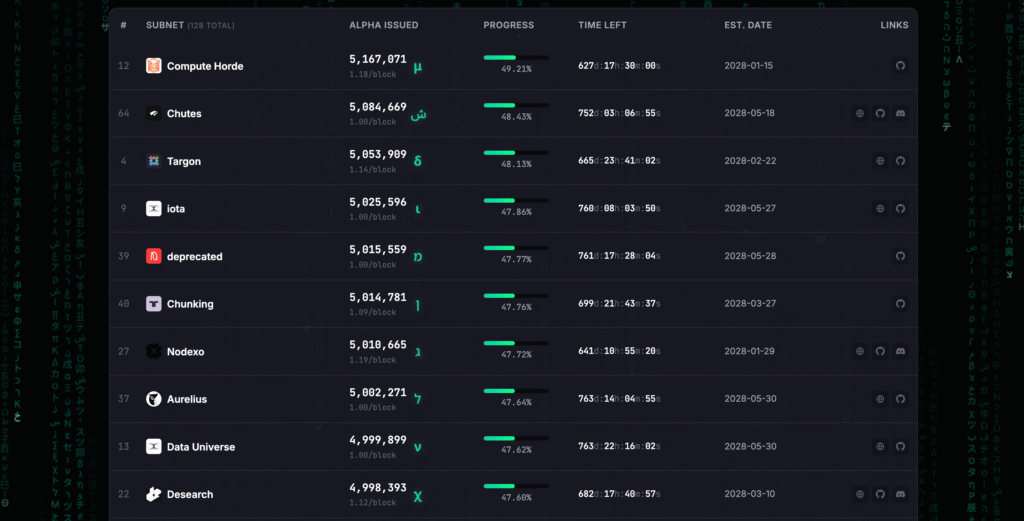

Bitcoin has one halving event every four years and the entire market plans around it. Bittensor has 128 halvings, each tied to a specific subnet hitting its 10.5M alpha cap, and almost no one is tracking the schedule.

Current halving progress on major subnets:

- Compute Horde (SN12): 48.89% to cap

- Chutes (SN64): 48.14%

- Targon (SN4): 47.82%

- IOTA (SN9): 47.58%

- Vanta (SN8): 46.89%

- BlockMachine (SN19): 46.42%

- Quasar (SN24): 45.73%

When each subnet hits 10.5M alpha, its emissions drop by 50%. The cluster of subnets sitting at 45–49% is the tell, and these aren’t isolated events. They’re going to roll through the network as overlapping supply shocks over the next 5–6 months.

Each halving makes the alpha for that subnet structurally scarcer, which strengthens the alpha/TAO ratio, which, back to Layer 2, pulls more $TAO into the subnet to buy now-cheaper-relative alpha. The loop tightens again.

Layer 5: Wallet Accumulation Is Quietly Accelerating

The flow off exchanges and out of root isn’t going into trading accounts. It’s going into cold storage and conviction wallets.

% TAO on Wallets:

- March 2025: 26%

- April 2026: 33.48%

A 7.48 percentage-point migration into self-custody in twelve months. That doesn’t look like retail rotation but more of a structural accumulation.

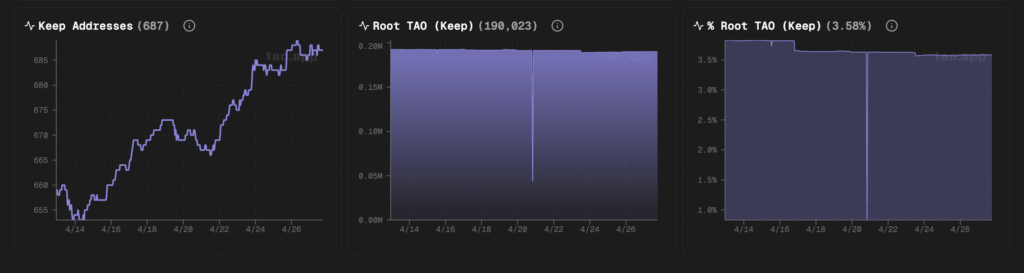

Keep Addresses (long-term holder wallets, defined as addresses that stake and don’t unstake):

- November 2024: ~100 addresses

- April 2026: 688 addresses

Nearly 7x growth in conviction holders in eighteen months.

And the most telling sub-metric:

- Root TAO (Keep): 190,042 $TAO

- % Root TAO (Keep): 3.58%

These are diamond-hands who staked and have never unstaked. Pure permanent lockup at the protocol’s most economically active layer. The trajectory is slow but extraordinarily one-directional.

Layer 6: The Sum of Alpha Prices = 1.36; A Mispricing in Plain Sight

This is the number that should make any subnet investor’s eyebrows climb.

128 subnets, each with independent alpha tokens, each freely tradeable against $TAO. The sum of every single alpha/TAO ratio across the entire network = 1.36.

In plain language: the entire alpha token market cap is only 1.36x the value of one $TAO.

That’s an astronomically mispriced discount sticker.

Either:

- The market is correctly pricing in that most subnets will fail (in which case the survivors are extraordinarily underpriced), or

- The market hasn’t woken up to subnet alpha as an asset class yet (in which case the entire alpha layer is mispriced).

Either resolution is bullish for $TAO specifically. Because the path to correcting that mispricing runs through buying alpha, and you buy alpha with $TAO. So the correction itself is a $TAO sink.

Why This Stacks Into a Spiral

Each layer in isolation is interesting. The thesis only becomes inevitable when you see how they interlock:

- Thin exchange supply means small flows move price hard.

- Reserve deficit keeps alpha structurally scarce relative to $TAO demand.

- Subnet migration moves $TAO into one-way sinks.

- Rolling halvings intensify alpha scarcity in waves over the coming months.

- Wallet accumulation removes free float from circulation entirely.

- Mispriced alpha creates a buy-side catalyst that itself consumes $TAO.

Every one of these dynamics strengthens the next one. There’s no layer that, when pressed, releases supply back to the market. Every release valve points the same direction: deeper into the protocol, longer in duration, more permanent in nature.

What This Means for the Subnet Economy

The bull case isn’t just for $TAO holders. It’s arguably stronger for subnet builders and alpha holders.

- Scarcer $TAO means each unit of subnet emission is denominated in a more valuable base asset.

- Subnets that survive their halvings emerge with a fundamentally tighter token economy.

- The 1.37 sum-of-alpha number suggests that quality subnets, the ones with real compute demand and real product traction, are trading at a fraction of fair value.

- As liquidity migrates from root to subnets, the subnets themselves become the primary venue for $TAO price discovery.

Bittensor isn’t just a token. It’s 128 token economies sharing a deflationary base layer with halvings staggered over months. That’s not a normal crypto setup. It’s closer to a network of mini-Bitcoins running on a substrate that itself behaves like Bitcoin, but with productive yield attached.

The Honest Caveats

No analysis is complete without the disclaimers, and credit to the original thread — this is an aggressive read of bullish data. Worth noting:

- Subnet economies are still young; many will fail, and failures could leak $TAO back to the market.

- Halving impact on alpha price is theoretical until it actually plays out.

- Crypto liquidity can dry up and expand violently; thin books cut both ways.

- The 1.36 sum-of-alpha figure could just as easily reflect that the market has correctly priced subnet risk.

None of this invalidates the thesis. It just means the spiral is a probabilistic structure, not a guaranteed outcome.

Charts and metrics referenced throughout: tao.app. Original analysis: Andy (@bittingthembits on X). This is commentary, not financial advice.

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment