In March, Philip Z. Maymin published the first serious academic study of how Bittensor subnet tokens behave as a financial market. He looked at 128 subnets across 406 trading days, from the dTAO launch in February 2025 through March 2026, and asked a simple question: are there patterns in how these tokens go up and down?

The answer is yes. And some of the patterns are surprising, while others are exactly what a careful look at the AMM math would predict.

Here are 10 things every Bittensor participant should take from this paper (and please note that none of the content of this article is financial advice).

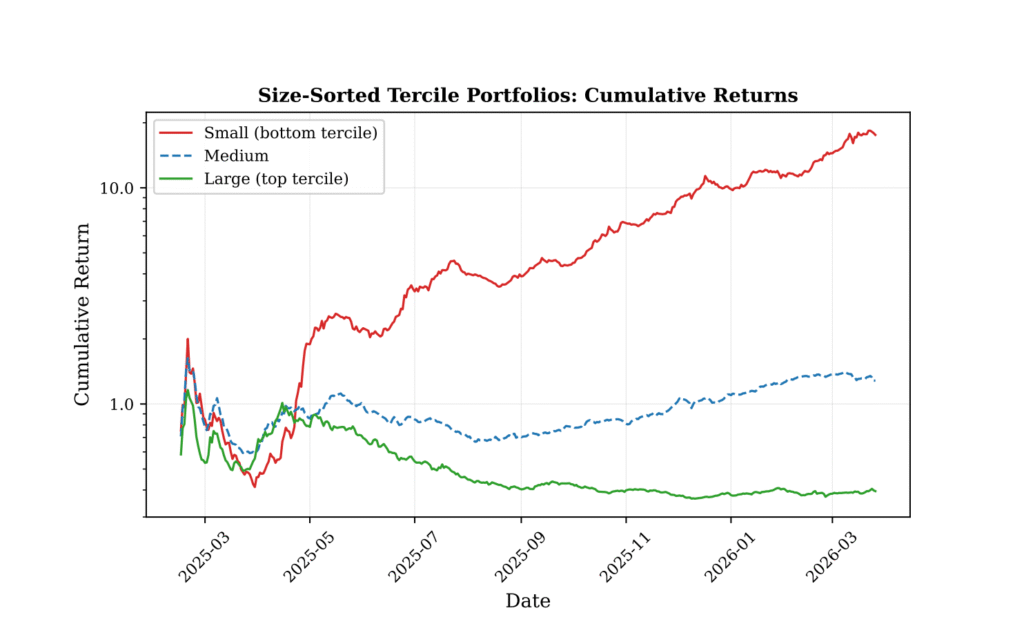

1. Small subnets have been crushing big subnets

This is the headline. The smallest third of subnets returned about 317% annualized. The largest third lost about 50%. If you split the universe into small, medium, and large, and just held the small bucket, you would have grown your stack roughly 25 times over the sample period. The large bucket would have lost you money.

A long-small / short-big strategy earned 1.01% per day on average.

2. This is not luck. It’s the math of the AMM.

Every subnet has a constant-product AMM pool holding TAO on one side and the subnet’s alpha tokens on the other. When emissions get staked into the pool, the percentage price jump depends on how big the pool already is. The same amount of TAO entering a small pool moves the price much more than entering a big pool.

So small subnets earn higher percentage returns from the exact same emission. Maymin proves this formally in his paper.

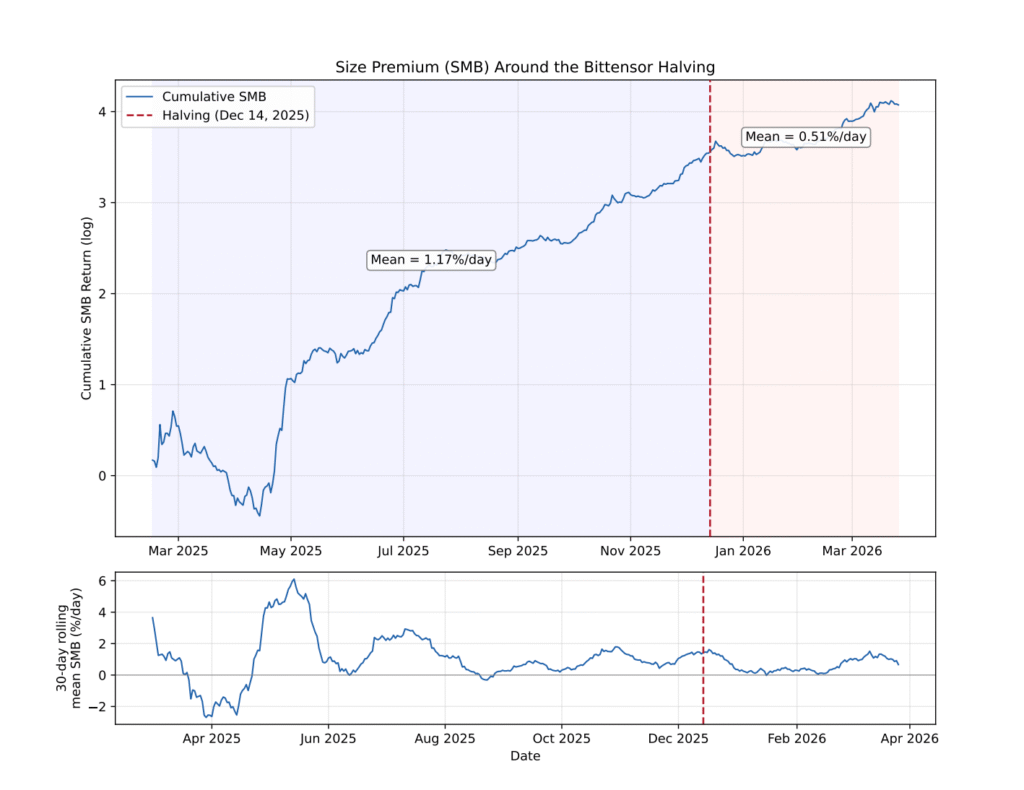

3. The December 2025 halving cut the size advantage almost exactly in half, as predicted

Before the halving, the small-minus-big return was 1.17% per day. After the halving, it dropped to 0.51% per day. The theory said it should drop by exactly half (because emissions dropped by half). It dropped by 0.44, almost spot on.

This is rare in finance. A theory made a precise number prediction, an independent research event tested it, and the number matched. That gives us a lot more confidence that the size effect is real.

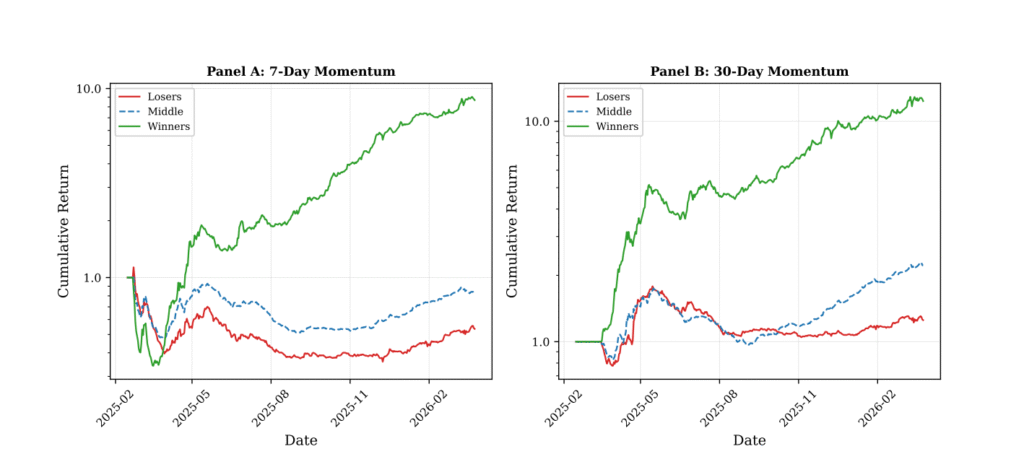

4. Momentum works on subnets, and winners keep winning

If a subnet has been going up over the past 7 days or 30 days, it tends to keep going up. A strategy of buying recent winners and shorting recent losers earned 0.75% per day at the 7-day horizon and 0.68% per day at 30 days.

5. Buying yesterday’s losers is a bad idea

Some traders try to “catch the bottom” by buying assets that fell yesterday. On Bittensor subnets, this loses money. The one-day reversal factor earned negative 0.86% per day. So past losers tend to keep losing, at least for a while.

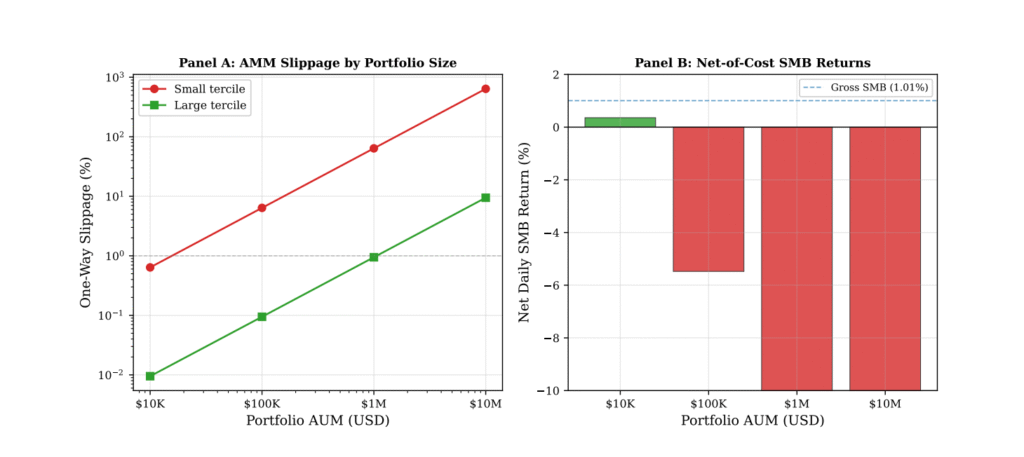

6. The strategy does not scale to real money

Here is the catch. Maymin calculates the exact slippage you would pay because the AMM math is transparent.

- At $10,000 in deployed capital, a small-minus-big strategy is still profitable (about 0.36% per day net of costs).

- At $100,000, transaction costs eat the entire gross return.

- At $1,000,000, the strategy is catastrophically unprofitable.

The median TAO reserves in small subnets is only about 540 TAO. Pools that thin cannot absorb six-figure trades without massive slippage.

7. The premium survives BECAUSE it doesn’t scale

This is the deepest insight in the paper. If the size premium were capturable by hedge funds, they would have already arbitraged it away. It still exists precisely because it lives in a liquidity niche too small for institutional money to enter.

Small participants have an edge here that large participants structurally cannot take from them.

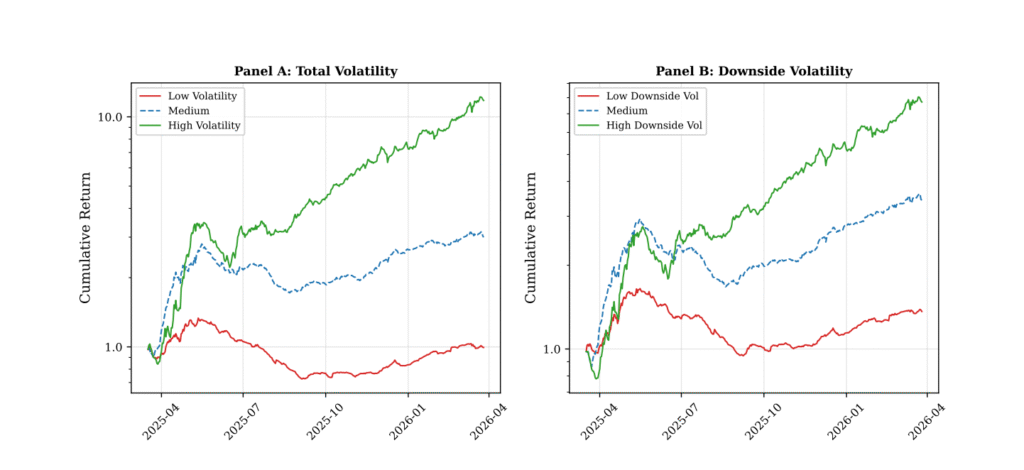

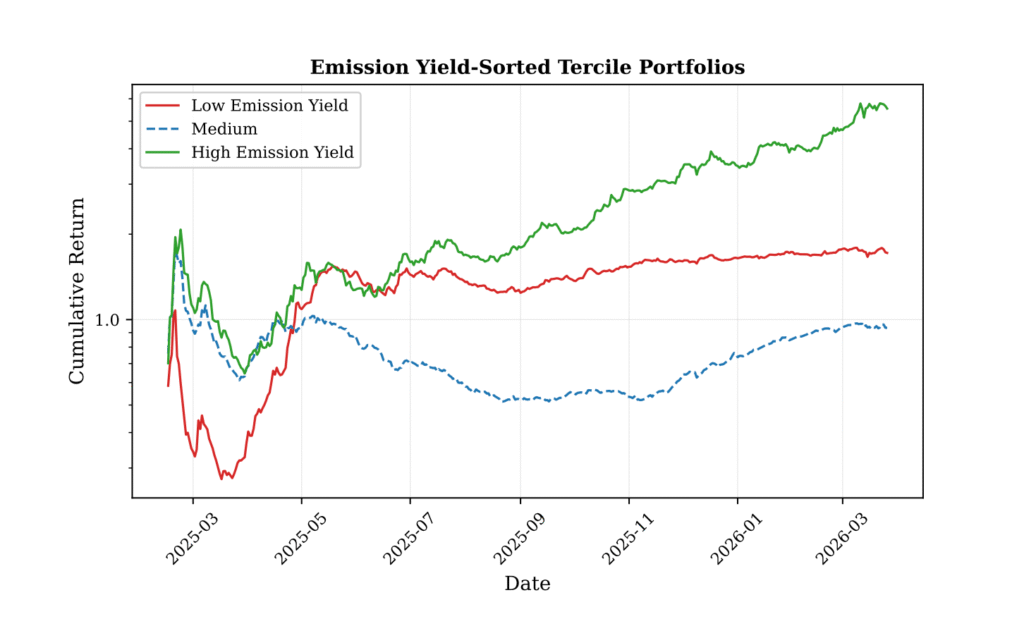

8. In subnets, risk and reward go together, but it’s an illusion

In stock markets, lower-volatility stocks usually outperform riskier ones (the “low-volatility anomaly”). On Bittensor subnets, the opposite is true: more volatile subnets earn higher returns. So do higher yield subnets. So do subnets with bigger downside swings.

But this is not evidence that markets are pricing risk well. It is the size effect wearing a costume. Small subnets are mechanically more volatile because the AMM amplifies price moves in thin pools. The correlation between the volatility factor and the size factor is 0.85.

So do not read this as “take more risk, get more return.” Read it as: small subnets are volatile by design, and that’s where the returns (including good APY) happen to be.

9. On Bittensor, size and liquidity are the same thing

In traditional finance, size and liquidity are related but separate. A mid-cap stock can be more liquid than a large-cap if it trades more often. On Bittensor, the AMM makes them mathematically identical: a subnet’s pool depth is a direct function of its market cap. The correlation between the size factor and the liquidity factor is 0.93, basically the same metric.

This means when people in the ecosystem talk about “small subnets,” they are also talking about “illiquid subnets.” The two concepts cannot be separated.

10. The whole asset class went up

Aside from all the factor stories, the simplest result of the paper is that holding an equal-weighted basket of every subnet earned 0.29% per day during the sample, with a reasonable Sharpe ratio of 1.35 in TAO terms. The broad subnet market appreciated, on top of all the relative effects between subnets.

What the paper does NOT prove

Honesty matters here. A few things to keep in mind before treating this paper as investment advice:

- The sample is only 13 months long. Patterns this clear in a short window may weaken over time.

- The cross-section is 128 subnets. This is modest compared to thousands of stocks in equity studies.

- New subnets tend to be small subnets, so part of the small-subnet return may come from an “IPO effect” rather than a permanent premium.

- The post-halving period also coincided with the move from price-based emissions to the flow-based Taoflow mechanism. The two effects are not perfectly separable.

- All returns are in TAO terms by default. TAO itself is volatile against USD. A robustness test in USD shows lower Sharpe ratios.

Maymin himself discloses that he is a co-owner of Djinn, a Bittensor project, which he names openly in the paper.

Why this paper matters

For two years, the Bittensor community has talked about the size advantage of small subnets informally. This paper turns that intuition into a measured, theory-backed, peer-review-ready finding. It also gives the ecosystem something it badly needs: a way of thinking about subnet returns that is not based on vibes, but on the actual AMM mechanics every participant interacts with.

The full paper is freely available on arXiv: arxiv.org/abs/2603.29751

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment