Zipcode (SN46)‘s leadership gave a technical breakdown of Bittensor’s Long/Short Mechanism, alongside a live announcement that Zipcode is dissolving all its subnet equity to move fully to a token-only capital structure. The long/short feature adds a hedging and enforcement instrument on top of the same $TAO-$ALPHA pools that already handle swaps, structurally different from anything on Solana or Ethereum.

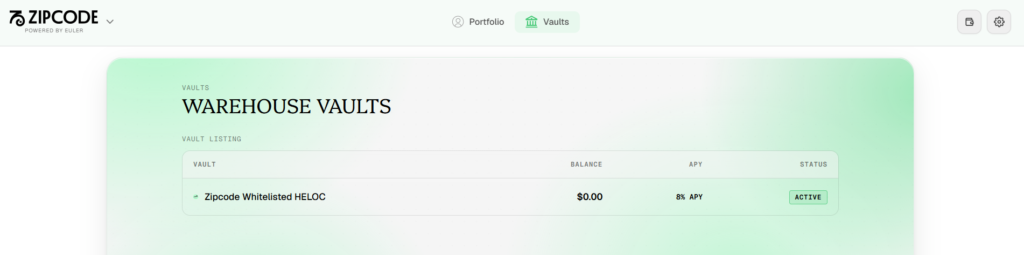

The equity dissolution is being pushed across Zipcode’s subnet portfolio, with the operating agreement being restructured so IP (Intellectual Property) and revenues route back to the token rather than to a separate equity layer. The conversation also previewed Zipcode’s RWA vaults targeting 6% to 8% conservative yield for institutional distribution.

Takeaways From the Space

The conversation moved between the mechanics, the trader and subnet-owner implications, and the Zipcode-specific announcements.

1. ONE POOL HANDLES BOTH SWAPS AND BORROWS

Lending on Solana or Ethereum requires separate protocols with fragmented liquidity. Bittensor uses the existing $TAO-$ALPHA pool as counterparty for perps and leverage, making the system more capital efficient than anything shipped elsewhere.

2. POSITIONS ARE $TAO AND $ALPHA NATIVE

Every long or short expresses a directional bet on subnet performance against $TAO, with no dollar-denominated version of the trade.

3. THE SHORT FLOW SETTLES AGAINST THE SAME POOL THE $ALPHA LIVES IN

A trader deposits $TAO, borrows up to roughly half in $ALPHA, and the pool sells those tokens into itself. Half of the $TAO stays in a settlement fund, and the other half decays over time at a set funding rate.

4. NO TRADITIONAL LIQUIDATIONS, ONLY FORCED CLOSURES

The pool closes positions when collateral runs out, producing cascading price movements in shallow pools because forced buyers push prices exponentially along the pool curve.

5. ‘LONG AND SHORT’ IS A HEDGING TOOL, NOT JUST DIRECTIONAL EXPOSURE

Every subnet stakeholder now has to think about hedging the way traditional finance operators do, with the same instruments running across traders, validators, and treasury operators.

6. EXTRACTIVE SUBNETS BECOME STRUCTURALLY SHORTABLE

If revenue is not cycling back into the token or validators are structural sellers, the mechanism gives holders a way to bet against that pattern directly.

7. WHALE ENFORCEMENT BECOMES A REAL MECHANIC

A large $TAO holder can short extractive subnets, extract $TAO from the pool back into their wallet, and act as a market moderator for the ecosystem. The framing across the Space was that the mechanism turns big holders into cops.

8. MANIPULATION VECTORS ARE REAL AND WORTH GUARDING AGAINST

Coordinated character assassination campaigns paired with large short positions could destroy subnets that do not deserve it. The counter is transparency tools that surface wallet clusters, forced-closure zones, and owner-wallet activity.

9. ZIPCODE IS DISSOLVING ALL ITS SUBNET EQUITY, PUSHED ACROSS THE PORTFOLIO

Zipcode’s $SN46 is confirmed, Ditto’s $SN118 is being pushed in the same direction, and all future capital raises will be for the token only. The operating agreement is being restructured so IP and revenues route back to the token, since any subnet with both equity and a token where equity captures value is structurally unstable under a shorting regime.

10. ZIPCODE’S RWA VAULTS TARGET 6% TO 8% YIELD FOR INSTITUTIONAL DISTRIBUTION

Real-world asset-backed credit products designed to sell into institutional allocators looking for on-chain yield with real-world backing rather than crypto-native inflation.

The vaults sit on top of the token-only capital structure as the distribution arm.

Sooner or Later, the Ball Doesn’t Lie

The conversation made the argument that Bittensor’s long/short mechanism is not just a financial primitive but a structural shift in how the network enforces accountability. Extractive designs get punished directly rather than waiting for deregistration, whales get a new lever to defend the ecosystem, and subnet owners lose the ability to hide behind a passive token model that captures value in equity while draining the alpha pool.

Zipcode’s equity dissolution is one team’s answer, betting that the subnets that compound over the coming cycles are the ones where every dollar of revenue and every unit of IP flows back through the token. The RWA vaults sit on top of that thesis as the institutional distribution arm, giving allocators a way to access Bittensor-backed yield through instruments they can already underwrite.

The question for anyone building on Bittensor over the next twelve months is no longer whether long/short arrives but which side of every position they end up on when it does.

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment