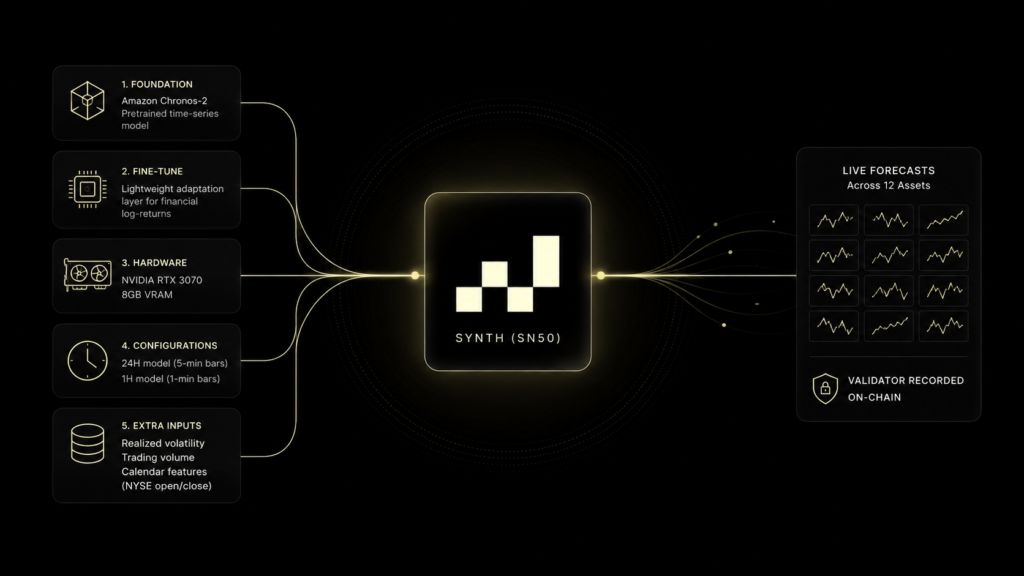

Synth (SN50) published its first research paper using the subnet as the benchmark for time-series forecasting in finance, applying Amazon’s Chronos-2 model to live price prediction across twelve assets on a single 8GB consumer GPU. All results are validator-recorded on-chain rather than self-reported, with two model configurations covering the subnet’s three competitions.

The setup uses a drift correction that removes directional bias from the central forecast while preserving the shape and uncertainty range that Synth’s scoring actually rewards. As of July 6, the miner ranks 36th by on-chain incentive across all three competitions, and the paper marks the first in a series that will use Synth as the reference benchmark for financial time-series research.

How The Model Runs

The miner starts with Amazon’s Chronos-2, a general-purpose time-series model, and adapts it to financial data using a small fine-tuning layer only a few megabytes in size.

1. The Foundation: Amazon’s Chronos-2, pretrained to handle time series across many domains.

2. The Fine-Tune: A lightweight adaptation layer that specializes the model for financial log-returns.

3. The Hardware: One NVIDIA RTX 3070 with 8GB VRAM handles training and live inference across all twelve assets.

4. Two Configurations: A 24-hour model on 5-minute price bars, and a 1-hour model on 1-minute bars for liquid crypto.

5. Extra Inputs: Recent realized volatility, trading volume where a reliable feed exists, and calendar features that tell the model whether the NYSE is open.

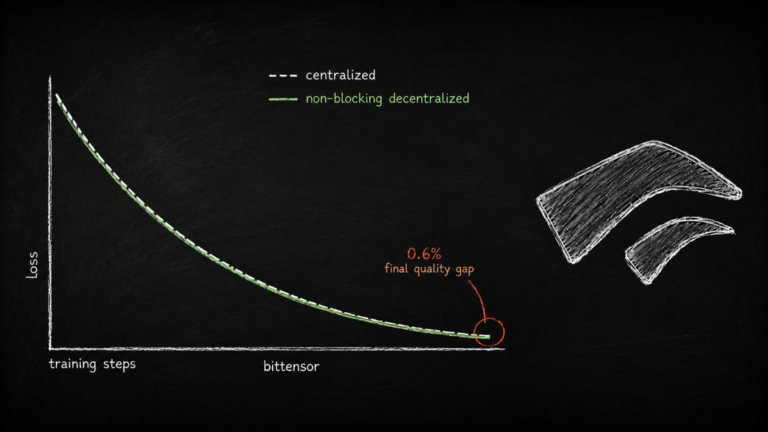

A consumer-grade GPU running a small adapter over a foundation model can produce forecasts competitive with far more expensive setups on a subnet paying real emissions for accuracy.

The Drift Correction

The most important design choice sits between the model’s raw output and the final forecast. Foundation models fed recent returns naturally extrapolate the trend, which turns the central forecast into an implicit directional bet that wins in trending markets and loses in reversals.

1. Directional tilt removed at inference. The miner strips the extrapolation bias from the central path.

2. Uncertainty range preserved. The forecast’s dispersion stays intact.

3. Tail behavior preserved. Fat-tail structure holds across every asset.

The central path now carries no directional view. What it carries is a calibrated probability distribution of what could happen, which is what Synth’s scoring actually rewards.

What the Model Emits

The forecasts show asset-appropriate behavior, which suggests the model is learning real market structure rather than just fitting numbers.

1. Volatility follows market hours. Tokenized stocks and WTI oil spike at the NYSE open around 14:30 UTC and collapse overnight. Crypto stays nearly flat around the clock.

2. Return distributions match asset classes. Crypto sits nearest to a normal distribution, while tokenized equities carry the fattest tails. SPYX shows excess kurtosis of 4.95, roughly 2.1x the Gaussian reference.

3. Tail structure ranks correctly. Crypto tail ratios sit at ~2.2 to 2.4, tokenized stocks reach 3.87, and every asset comes in above the Gaussian baseline of 1.82.

4. Horizon growth is well-behaved. Uncertainty grows with the square root of time, close to a random-walk reference on log-log axes.

The paper flags two caveats: The sampled increments are bounded by the model’s predictive range, so this is not an unbounded-tail claim, and Pooling across steps inflates the tail measurements, so the reported numbers overstate the per-step tail behavior. The ordering across assets is still genuine.

Where This Sits in the Broader Synth Thesis

The paper is the first output of the pivot Synth announced earlier this month, where the subnet restructured itself as a research engine using live financial markets as the benchmark for time-series models.

The miner documented here is a working example of what that competition produces. A consumer GPU running a fine-tuned foundation model against on-chain validator scoring, competing across three contests and producing forecasts that show sensible market behavior across twelve assets.

The 36th rank is actually not the story, it is that Synth is now shipping papers that use the subnet as their benchmark, which is exactly what turns a competition into a research institution. More papers follow in the series.

➛ Read the Full Paper Here

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment