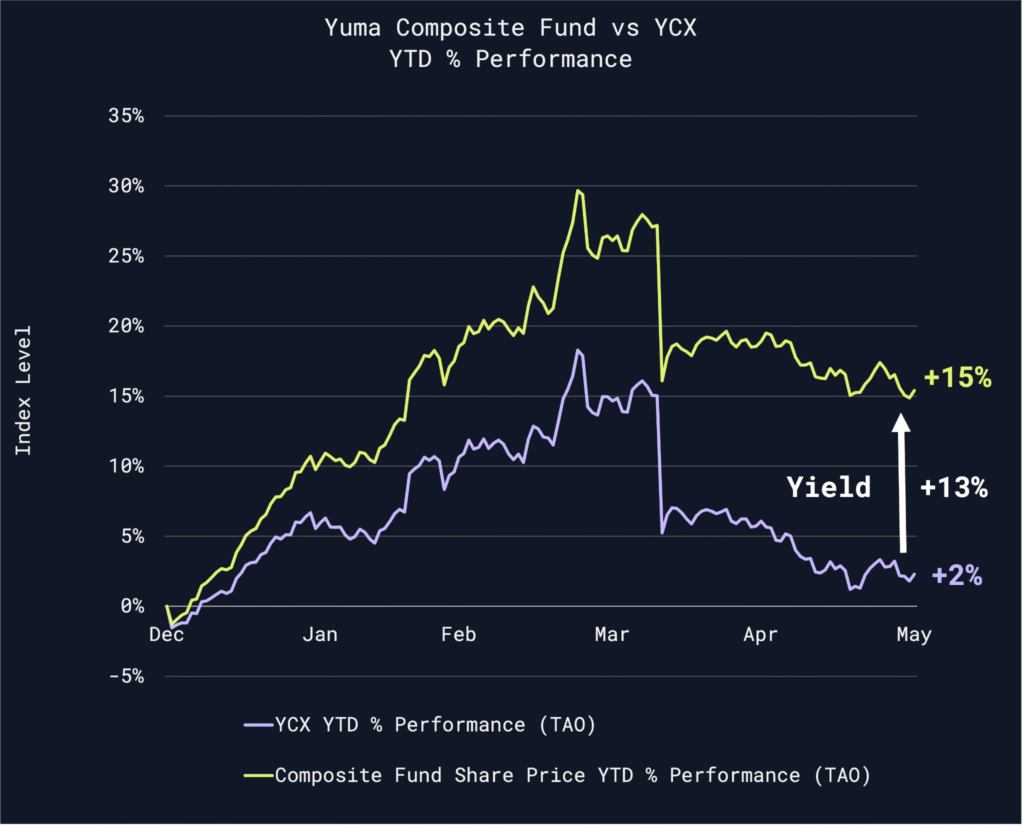

Yuma published an update showing that its Composite Fund has outperformed the Yuma Composite Index (YCX) by +13% year-to-date as of May 31.

The YCX captures price movements across the Bittensor subnet ecosystem on a market-cap-weighted basis, while the Composite Fund reflects full token economics including yield generation on top of price exposure.

Year-to-date, the estimated Composite APY (Annual Percentage Yield) has ranged between roughly 35% and 55%, which is the yield component driving the outperformance. The 13% gap is not a price call but the difference between holding the index passively and earning the yield the same positions generate when held actively.

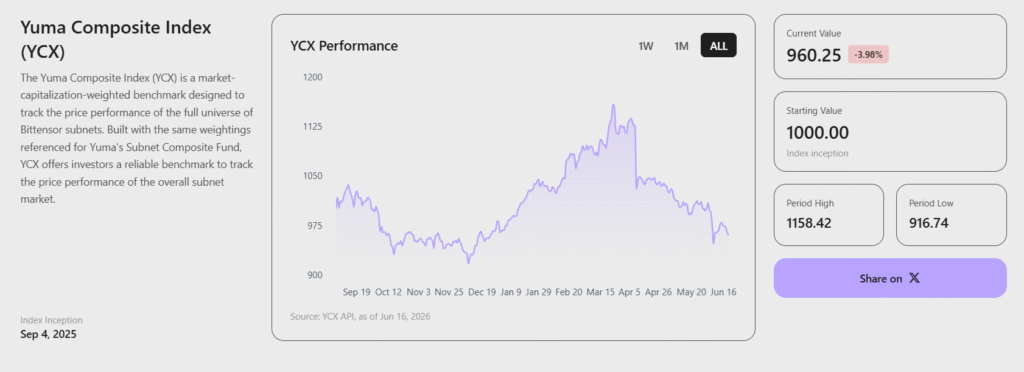

What YCX Measures

YCX is constructed to function like a traditional equity index for the Bittensor subnet ecosystem, which is why this comparison is fair:

1. Market-Cap Weighting: Larger subnets carry more weight in the index, similar to how the S&P 500 and other mainstream equity indices are built.

2. Reflects Both Price and Issued Supply: Movement in either dimension shows up in the index.

3. No Artificial Step Changes: New subnet registrations do not create discontinuities in the index value.

The contrast with a simple sum of subnet token prices is significant. Simple sums overweight smaller tokens by giving a $1 token the same influence as a $1,000 token, and they introduce step changes every time a new subnet is registered. YCX avoids both distortions and measures the ecosystem the way a fund manager actually thinks about it.

Why the Composite Fund Wins

The mechanical answer to why the Composite Fund beats YCX is yield. The strategic answer is that yield is the part of subnet ownership that gets ignored in pure index tracking.

1. YCX is Price-Only Exposure: It tracks where prices go but does not capture the yield that subnet positions generate alongside price movement.

2. The Composite Fund Captures Both: Same subnet exposure, with the yield component compounding on top of the price movement.

3. The APY Band Tells The Story: Even at ~35% APY, held positions generate meaningful returns separate from price action. At ~55%, the yield by itself rivals what most equity strategies target as total return.

The takeaway here is that subnet token ownership has two return streams (price and yield), and treating it as a single-stream exposure leaves significant return on the table.

YCX is the right benchmark for tracking subnet ecosystem price movements at the institutional level. The Composite Fund is the structured way to harvest both streams together.

The 13% YTD outperformance is where the gap stood as of May 31, with the yield component running at 35-55% APY through that period.

None of this is investment advice, and past performance is not a guide to future results, but for anyone holding subnet positions and wondering whether the yield side is meaningful, the data says it is doing real work.

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Enjoyed this article?

Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox — every morning before markets open.

Be the first to comment