As Bittensor continues to grow into one of the most closely watched decentralized AI networks, questions around its early token distribution and ownership structure have naturally intensified.

Much of the speculation centers on familiar concerns within crypto markets, including premine allocations, venture capital influence, and exchange-held supply. However, according to Jacob “Const” Steeves, co-founder of Bittensor, the reality behind $TAO’s distribution follows a fundamentally different model, one rooted in work, open markets, and competitive issuance rather than preferential allocation.

His clarifications provide a more precise view into how $TAO entered circulation, how early capital was raised, and what role external entities have played in the network’s development.

No Premine, No Preferential Allocation

A central point of clarification is that Bittensor did not follow the traditional path of premining tokens for insiders or venture capital firms.

Instead, the issuance model was designed around a simple principle:

a. All $TAO was mined,

b. No tokens were created or reserved in advance, and

c. No allocations were granted for free to insiders or investors.

This distinction is critical because it establishes that every unit of $TAO in circulation originated through participation in the network, rather than through early distribution mechanisms that often concentrate ownership.

As Const emphasizes, the system was intentionally structured so that every token is tied to work performed under competitive conditions, reinforcing the broader goal of aligning incentives with contribution.

OTC Sales: How Early Capital Entered the System

While there was no premine, Bittensor did engage in over-the-counter (OTC) token sales during its early stages, specifically between 2021 and 2023.

These sales were not distributions of newly created tokens, but rather transfers of tokens that had already been mined by the founding team.

On the OTC sales:

a. Approximately 600,000 $TAO was sold,

b. Buyers included Firstmark, Digital Currency Group (DCG), and Polychain,

c. Sales occurred over a multi-year period from 2021 through 2023, and

d. The tokens originated from personally mined supply, not reserved allocations.

The capital raised through these transactions played a direct role in building the organization behind Bittensor, particularly in supporting the development of the team associated with the Opentensor Foundation (OTF).

Pricing and Long-Term Alignment

The average price for these OTC transactions was reported at $18 per $TAO. From the perspective of the founding team, these sales represented a mutually beneficial exchange, providing early funding while offering long-term exposure to participating entities.

At the same time, Const acknowledges that these entities have operated independently in managing their holdings:

a. Some have sold portions of their positions over time,

b. Sales have occurred in tranches rather than a single exit, and

c. Continued participation or exit remains entirely at their discretion.

This reinforces the idea that, despite early involvement, these entities do not possess structural control over the network, and instead function as market participants like any other holder.

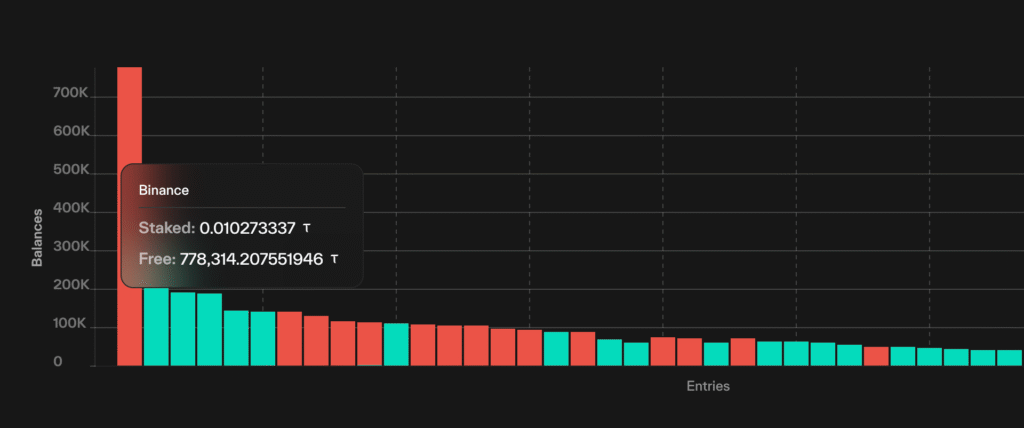

CEX Holdings: Understanding Exchange Balances

Another point of confusion relates to the presence of a significant amount of $TAO on Binance, which has been interpreted by some as exchange ownership. It was clarified that this interpretation is incorrect.

On the holdings on CEX (Centralized Exchanges) like Binance:

a. The tokens are not owned by Binance itself,

b. They are held in individual user accounts on the exchange, and

c. The balances reflect users transferring $TAO to Binance, not allocations to the platform.

This distinction is important because exchange balances often appear as concentrated holdings, even though they represent distributed ownership across many participants.

The Core Philosophy: Work, Competition, and Open Markets

Underlying all of these decisions is a consistent philosophy that has guided Bittensor’s development from the beginning. The principles guiding $TAO distribution is that:

a. No Free Allocations: Every token must be earned or acquired through market participation,

b. Work-Based Issuance: Mining is directly tied to contribution within the network,

c. Competitive Dynamics: Participants must compete to earn rewards, and

d. Open and Transparent Markets: Price discovery and ownership evolve freely over time.

This framework reflects a deliberate attempt to align token distribution with the broader mission of decentralized AI, where value is created through participation rather than granted through access.

A Different Model of Distribution

In an ecosystem where early token allocation often defines long-term power structures, Bittensor presents a model that departs from conventional patterns. There was no premine, no preferential allocation to venture capital, and no structural advantage embedded into the token’s origin.

Instead, early funding was achieved through the sale of mined tokens, ownership remains fluid within open markets, and all participants, regardless of entry point, operate under the same fundamental rules.

This resulted in a system where $TAO is not distributed by permission, but by participation, and where value is not assigned, but earned.

As the network continues to evolve, these early design choices remain central to understanding both its current structure and its long-term trajectory.

Enjoyed this article? Join our newsletter

Get the latest Bittensor & TAO ecosystem news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Be the first to comment