When Gordon Frayne sat down with Erkin Kamran (founder of 0xMarkets), the conversation quickly moved past surface-level DeFi narratives into something more grounded. This was not about building another exchange, it was about translating decades of institutional market structure into an on-chain system that can actually compete.

Erkin, drawing from years in traditional finance and high-volume trading infrastructure, made the direction clear early. The goal with 0xMarkets is not to reinvent trading, but to rebuild it properly on-chain, anchored on efficiency, cost realism, and scalable liquidity.

That is exactly where Cartha, Subnet 35 on Bittensor, comes in.

From TradFi to On-Chain: Building What Actually Works

Gordon opens by anchoring the conversation in Erkin’s background, and it becomes immediately obvious why this approach feels different.

Erkin explains that his experience spans:

a. Institutional FX (Foreign Exchange) markets and low-latency trading systems,

b. Building matching engines and execution infrastructure,

c. Scaling platforms to billions in monthly trading volume, and

d. Designing brokerage systems across global markets.

That experience shapes the core thesis behind 0xMarkets. As Erkin puts it during the discussion, the opportunity is not in competing with existing crypto-native platforms on hype, but in targeting a much larger and often ignored market:

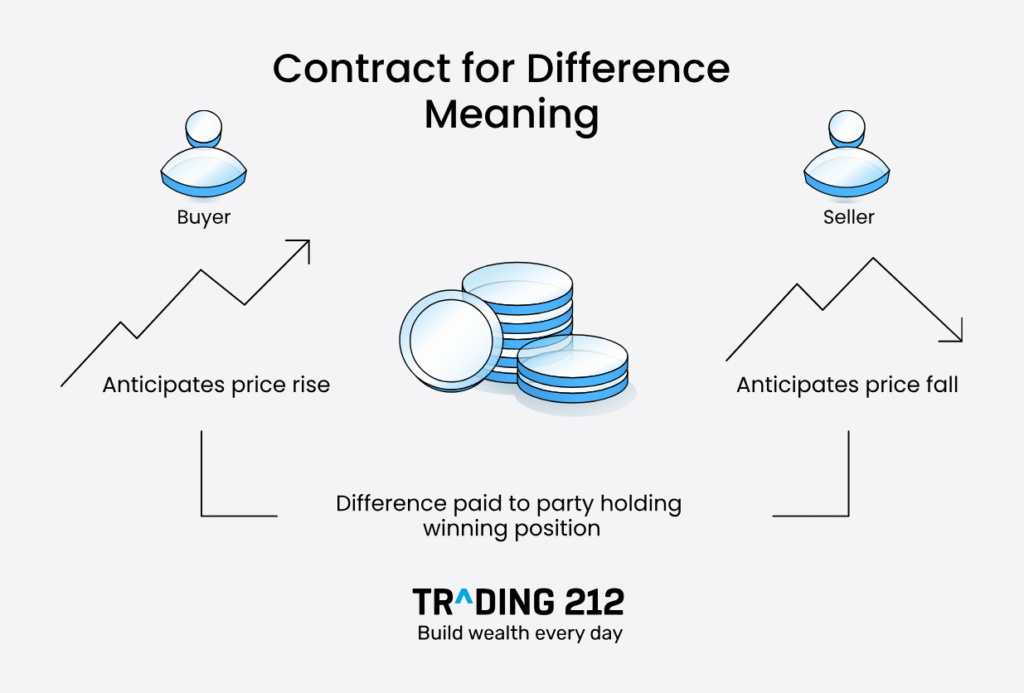

a. The CFD (Contract for Difference) market, processing over $1.2 trillion daily volume,

b. Dominated by centralized brokers with highly efficient cost structures, and

c. Still largely disconnected from DeFi.

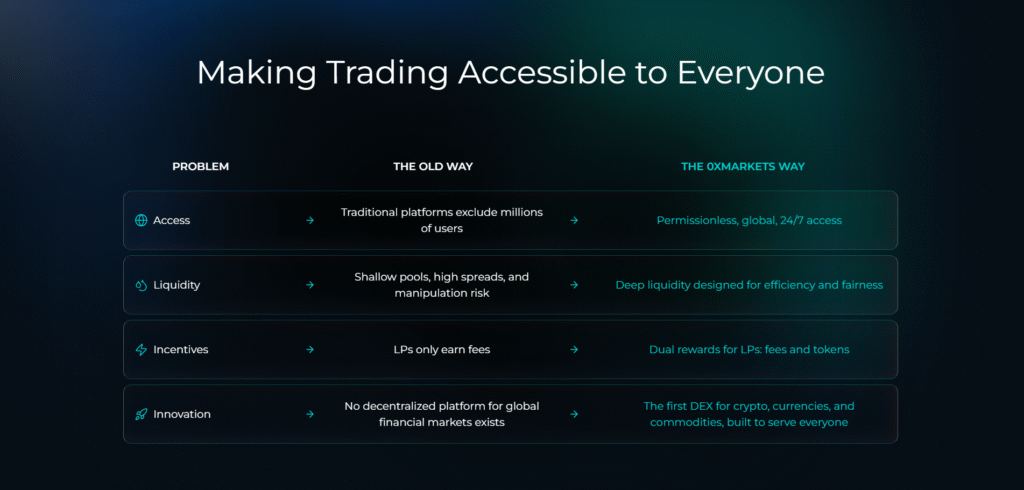

This is where the gap lies. While platforms like Hyperliquid have proven demand for on-chain trading, Erkin makes a critical distinction. Most existing solutions are optimized for crypto-native users, not for traders accustomed to tight spreads and low execution costs.

0xMarkets is designed to close that gap.

The Product Stack: Liquidity Engine Meets Exchange Layer

Gordon transitions the conversation toward product, and Erkin breaks the architecture into two clear layers:

a. Liquidity Engine (on Bittensor via Cartha), and

b. Exchange Layer (execution environment).

The liquidity engine is already live on mainnet and actively bootstrapping capital, while the exchange interface is currently running on testnet with live trader participation.

In all, it allows 0xMarkets to:

a. Build and scale liquidity independently,

b. Test execution environments without risking core infrastructure, and

c. Align incentives directly with contributors in the network.

In the ecosystem, early traction is already visible., and as it was pointed out, liquidity has grown rapidly, with strong participation from early providers.

Competing Where It Matters: Cost, Market Fit, and Scale

One of the most direct moments in the conversation comes when Gordon asks the obvious question: Why would a trader choose 0xMarkets over something like Hyperliquid?

Erkin answers without hesitation, and the response is rooted in economics rather than ideology. He opined that for a standard gold trade:

a. Centralized brokers: ~ $50 cost,

b. Existing DeFi platforms: ~ $1000 cost, and

c. 0xMarkets target: ~ $150 cost.

Rather than chasing extremes, 0xMarkets aims to sit in the middle, offering:

a. Lower costs than decentralized competitors,

b. Better user control than centralized platforms, and

c. A realistic premium justified by self-custody and transparency.

But cost is only one side of the equation, Erkin emphasizes that product-market fit is equally critical, and traders used to traditional systems expect:

a. Familiar asset classes such as FX, commodities, and indices,

b. Deep liquidity and reliable execution, and

c. Consistent pricing without extreme slippage.

This is why the initial rollout focuses on major assets (like Bitcoin, gold, and FX pairs), high-demand markets with proven trading activity, and gradual expansion into niche and emerging market assets.

The strategy is deliberate as the ecosystem is starting where liquidity already exists, then expanding outward.

Liquidity Mining: A Different Model of Participation

Gordon then shifts into one of the most important aspects of the system: liquidity provisioning. Unlike typical DeFi models, Cartha simplifies participation significantly.

With it, liquidity providers, deposit $USDC only, avoiding exposure to volatile token pairs, act as counterparties to trader positions, and earn from multiple aligned revenue streams

Erkin outlines the structure clearly, noting that:

a. 100% of trading PnL (Profit and Loss) and spreads go to liquidity providers,

b. 31% of token emissions are distributed based on contribution, and

c. 50% of platform fees are shared with liquidity providers.

This creates a layered reward system that combines real trading activity, protocol emissions, and fee-based income.

Gordon highlights the current yields, noting strong early returns driven by emissions, while Erkin explains how this evolves over time.

As trading volume increases:

a. Fee revenue becomes dominant,

b. Emissions become a smaller component, and

c. Yield transitions from inflation-driven to activity-driven.

It is a classic bootstrapping curve, but executed with clarity.

Incentives, Governance, and the $SN35 Flywheel

The conversation then moves deeper into token mechanics, where Erkin introduces the $veALPHA system. These tokens are not just rewards, they are:

a. Yield-bearing assets,

b. Governance tools, and

c. Drivers of long-term alignment.

The fee distribution model is structured as:

a. 50% to liquidity providers,

b. 40% to $veALPHA stakers,

c. 10% to the protocol, and

d. Optional allocation for buyback and burn.

What makes this dynamic is governance because $veALPHA holders can vote on fee redistribution, adjust buyback mechanisms, and influence long-term token economics

And importantly, rewards can be received in $USDC for stability, and $SN35 tokens for compounding exposure.

As Erkin explains, if users choose $SN35 rewards, the system actively buys tokens from the market, reinforcing demand and creating a feedback loop.

Scaling the System: From Retail to Institutional Liquidity

As the discussion progresses, Gordon brings up scalability, and this is where the long-term vision becomes clearer. Erkin outlines a phased approach:

a. Start with liquidity pools to bootstrap participation,

b. Transition toward hybrid models, and

c. Introduce institutional market makers over time.

The goal is not just to attract users, but to build a system capable of handling:

a. Large-scale trading volume,

b. Institutional-grade liquidity, and

c. Millions of active users.

This includes future upgrades such as order book integrations, improved market-making infrastructure, and enhanced liquidity depth.

At the same time, user experience remains a priority. Planned improvements include:

a. Social wallet integrations,

b. Gasless transactions,

c. Fiat on-ramps and off-ramps, and

d. One-click trading flows.

As Erkin puts it, the platform should not require deep Web3 knowledge to use.

Closing Perspective: A Market Too Large to Ignore

As the conversation wraps, Gordon brings it back to the bigger picture, and Erkin leaves one final point that anchors everything. The market 0xMarkets is targeting is not small.

It is massive, fragmented, and still largely untouched by decentralized systems, and that creates an unusual opportunity.

Rather than competing for the same users, 0xMarkets is positioning itself to expand the total addressable market for on-chain trading, bringing in participants who have never used DeFi before.

The model is simple to access, but powerful within with lower costs than existing DeFi platforms, better incentives than centralized systems, and infrastructure designed for real scale.

In a space often driven by narratives, this approach stands out because it is grounded in something much harder to fake: Real market structure, real liquidity, and real demand.

This combination does not just compete, it compounds.

Enjoyed this article? Join our newsletter

Get the latest TAO & Bittensor news straight to your inbox.

We respect your privacy. Unsubscribe anytime.

Be the first to comment