A single research note was enough to rattle the market. When Citrini Research published its scenario titled “The 2028 Global Intelligence Crisis,” it sketched a future where artificial intelligence does not just disrupt industries. It destabilizes demand itself!

The reaction was almost wild as commentators debated it, equities dipped, and narratives spread.

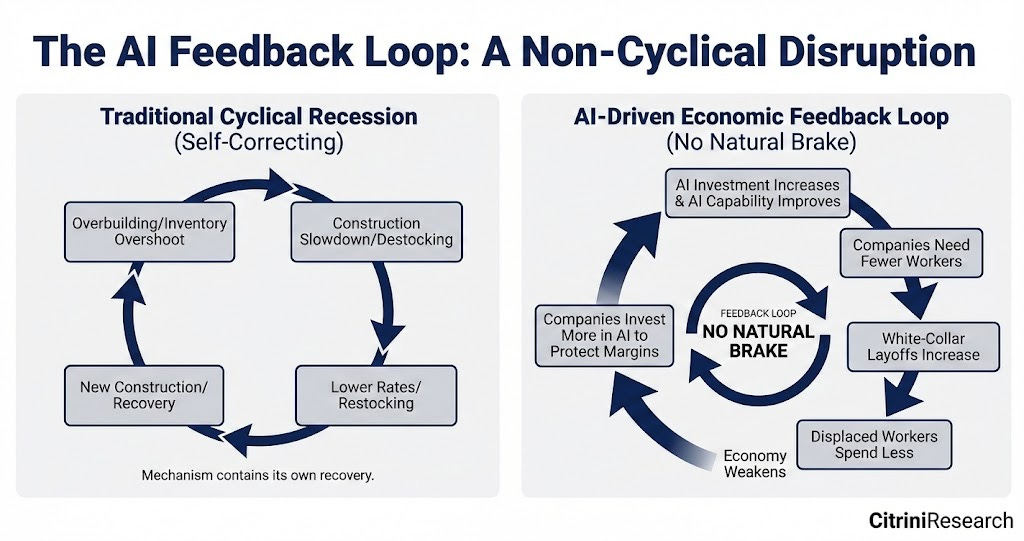

The premise was that AI gets better and cheaper, and the effect would be that companies cut white collar jobs, due to which household income falls, demand would weaken, margins compress, firms would continue to double down on AI to protect profits, and more jobs would disappear. It’s just a self-reinforcing loop.

The report called the end state “Ghost GDP,” during which profits rise, productivity looks strong, output prints on paper, but the money stops circulating through people.

That is the fear. Not a recession driven by credit, not even a financial crisis driven by leverage, but a demand crisis driven by automation.

Whether you believe that scenario or not, it surfaces a deeper structural question: If AI becomes the dominant productive force in the economy, who captures the upside?

The Ghost GDP Problem

The Citrini framework is a scenario that highlights something real. AI does not behave like past technologies in one key respect: It does not just augment labor. In many domains, it, in fact, substitutes for cognitive work directly.

If that substitution scales faster than new categories of employment emerge, you could see:

a. Rising structural unemployment,

b. Concentrated corporate profits,

c. Productivity gains that do not translate into wage growth, and

d. Lower aggregate consumption.

That is what “Ghost GDP” implies. Output exists, so does profits exist, but circulation weakens.

Economists can argue Say’s Law, optimists can point to historical precedents where technology ultimately created more jobs than it destroyed, and both arguments have merit.

However, neither addresses the ownership layer, because the core issue is not whether AI increases output, but who owns the machine.

Automation Is Not the Enemy; Concentration Is

Every industrial leap displaced labor at first. The difference today is capital intensity and ownership concentration.

Frontier AI systems are expensive to train, expensive to scale, and increasingly controlled by a narrow set of actors. If those systems become the backbone of global productivity, then their economics determine how value flows.

There are two paths:

a. AI becomes a centralized profit engine, and

b. AI becomes a distributed economic network.

In the first case, productivity gains accrue to a small cluster of firms and shareholders. In the second, participation is open, and rewards are market coordinated.

This is where crypto enters the conversation.

A Different Settlement Layer for Intelligence

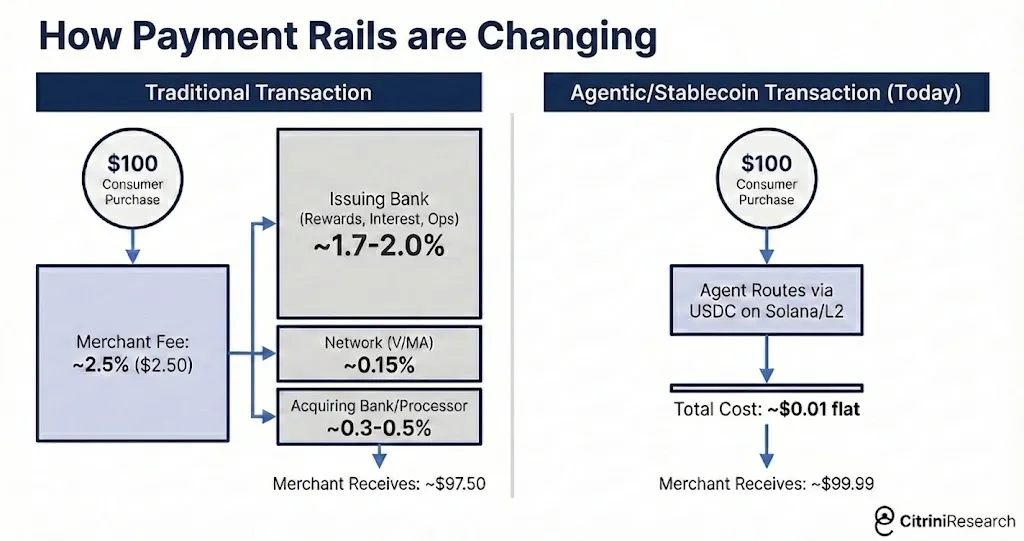

If AI agents transact, coordinate, and produce economic value autonomously, they require a monetary and settlement layer that operates continuously and globally. A 24/7 machine economy does not settle well on legacy banking rails; it settles on crypto.

It needs a system designed specifically to coordinate intelligence production itself. That is the thesis behind Bittensor and its native asset, $TAO.

Bittensor reframes AI not as a product owned by a corporation but as a network owned by participants.

How Bittensor Changes the Everything

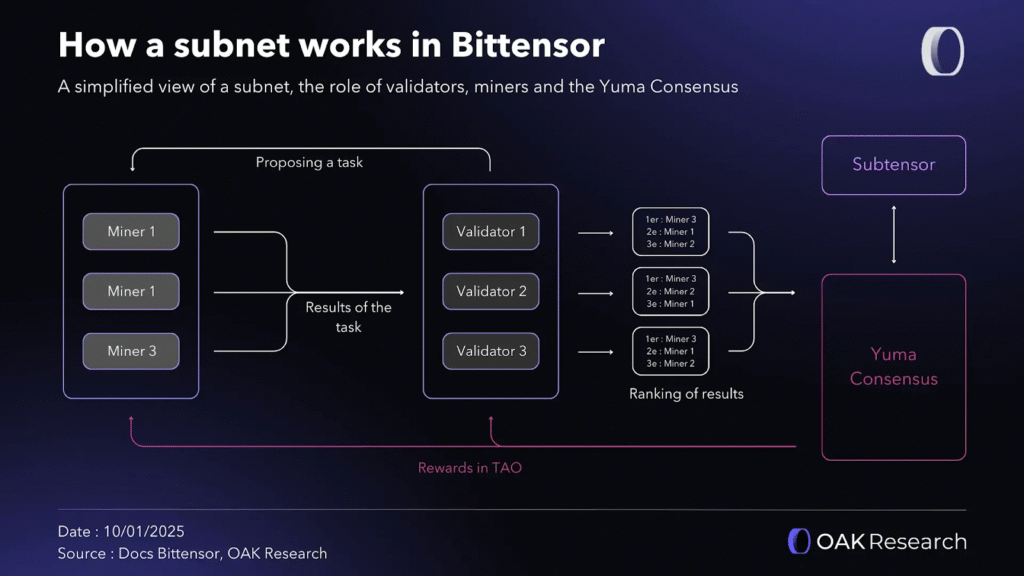

Bittensor turns machine learning into a competitive, incentive-driven marketplace. Instead of one company training a model behind closed doors:

a. Miners produce machine learning outputs (intelligence).

b. Validators evaluate quality.

c. Emissions reward performance.

d. Capital flows through decentralized actors.

This results in an open intelligence economy where contributors are paid directly in $TAO.

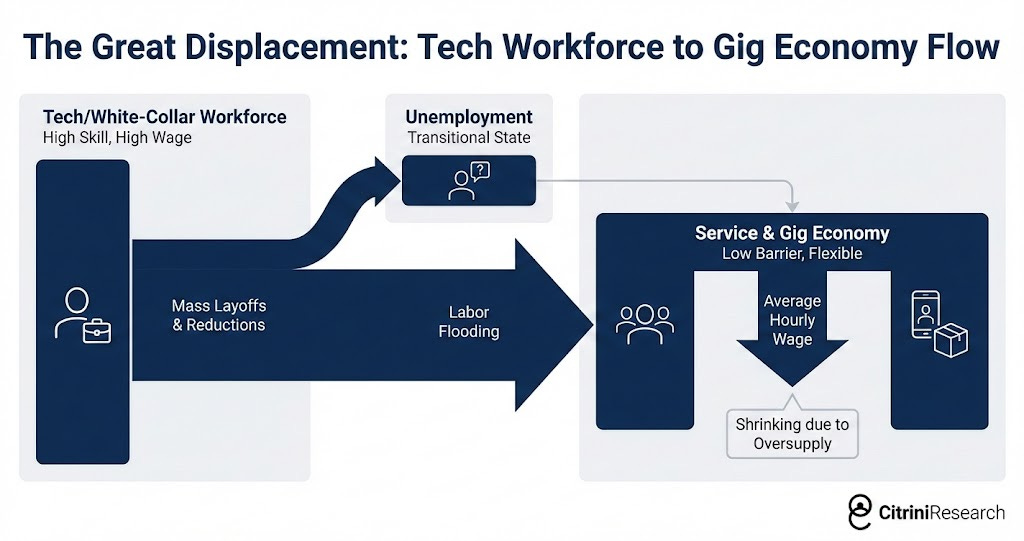

In the ‘Ghost GDP’ debate, this matters not only because AI can dispose labour, but because through this infrastructure labour (individuals) can:

a. Contribute compute

b. Provide models

c. Validate outputs

d. Launch specialized AI subnets

Then they are not merely displaced workers, they are participants in a global machine economy where ownership broadens, and upside distributes. As the intelligence of Bittensor scales, there are emergence of subnets that solve this specific problem. Handshake (subnet 58) is building the “Trust Action Layer”, a decentralized payment and verification protocol that gives AI agents their own wallets, allowing them to transact with the world seamlessly, permissionlessly, and instantly.

The Incentive Architecture

Unlike traditional AI firms where equity is concentrated, Bittensor’s structure ties value accrual to network contribution. $TAO functions as:

a. The staking asset securing validation,

b. The emission base funding innovation,

c. The settlement currency across subnets, and

d. The index of aggregate network value.

As intelligence production scales, demand for $TAO scales with it. This mechanism creates a structural link between AI growth and token value.

In a world where AI agents transact with each other, $TAO becomes more than a speculative asset. It becomes infrastructure.

If the Doom Loop is Even Partly True

Let us assume the Citrini scenario is directionally correct. If:

a. AI meaningfully compresses white-collar employment,

b. Corporate profits remain strong, and

c. Productivity rises while wage growth lags.

Then the question becomes how individuals access the value layer of automation. Traditional equities offer one path, but equity ownership remains uneven and mediated.

Crypto networks offer another through open participation, programmable incentives, and global settlement. Then, Bittensor ($TAO) goes a step further. It does not just tokenize AI companies. It tokenizes intelligence production itself.

That is a structural difference.

This Is Not About Stopping AI

AI will not slow down because markets fear it; companies, as well, will not avoid automation to preserve macro balance. The trajectory is clear: AI gets cheaper, capabilities improve, and adoption widens.

The real choice is architectural, because questions on what to build erupts. Like, do we build:

a. Closed AI systems that concentrate returns, or

b. Open AI networks that distribute them.

Bittensor represents a bet on the second path.

The Bigger Picture

Markets will continue to oscillate between euphoria and panic, research notes will circulate, headlines will amplify worst-case scenarios, but beneath the noise lies a simple economic truth. This truth is that technology does not inherently destroy economies; it redistributes power.

If AI becomes the dominant productive force of the next decade, the defining question will not be whether GDP grows; it will be who participates in that growth.

Ghost GDP is only a threat if value accrues to machines owned by the few. If intelligence becomes a network owned by many, the narrative changes entirely.

And that is where $TAO enters the macro conversation, not as a hedge against AI, but as a structural claim on its expansion.

Be the first to comment